May 11, 2026

Key Points:

● Unexpected bonuses can be used strategically instead of spent impulsively.

● Short-term bond ladders provide liquidity while preserving capital.

● Staggering bond maturities allows for regular access to funds.

● Even modest returns from bonds can outperform idle cash accounts.

● Planning ahead ensures windfalls support long-term financial stability.

Estimated Reading Time: 8 minutes┃Post by: Evelyn Hartman

Introduction: Transforming Windfalls into Financial Tools

Receiving a work bonus out of the blue can feel exhilarating. Perhaps it’s a $5,000 holiday bonus or a surprise end-of-year payout. The immediate temptation is to splurge—new gadgets, vacation upgrades, or fine dining. However, turning that windfall into a short-term bond ladder can preserve capital, provide modest returns, and maintain liquidity for emergencies. This approach allows professionals to balance the excitement of a sudden cash influx with practical financial foresight.

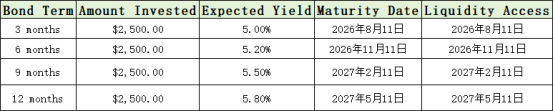

Imagine receiving a $10,000 bonus. Instead of spending it, you could allocate it across a series of three-, six-, nine-, and twelve-month bonds. Each bond matures at a different time, allowing you to access funds in intervals while earning interest along the way. This simple structure prevents impulsive spending and keeps your money working even in the short term.

How Short-Term Bond Ladders Work

Short-term bond ladders are straightforward in principle: divide your capital into equal portions and invest in bonds with staggered maturities. For instance, using the $10,000 example:

This structure creates predictable access to funds, ensuring that part of your windfall is always available without having to sell assets at unfavorable times. Real-life applications of this method show that even conservative short-term bond investments can outperform traditional savings accounts, which often yield minimal interest while leaving money idle.

Consider a scenario where you encounter an unexpected car repair or medical expense. With a bond ladder, a portion of your bonus matures exactly when you need it. Contrast that with keeping the entire bonus in a checking account, earning nearly zero interest while still being vulnerable to impulsive spending. The ladder approach balances liquidity, stability, and incremental growth.

Why “Bonus Segregation” Works Better Than Traditional Budgeting

One overlooked advantage of using a short-term bond ladder for work bonuses is psychological separation. Behavioral finance studies consistently show that people treat “extra” income differently from salary income. Annual bonuses, retention incentives, stock vesting payouts, and unexpected commissions are often mentally categorized as “free money,” which increases the likelihood of discretionary spending.

By immediately allocating bonus money into staggered fixed-income instruments, professionals create a friction barrier between themselves and impulsive consumption. Financial planners sometimes call this “forced intentionality.” Instead of debating whether to spend the money every weekend, the funds are already assigned to a structured liquidity system.

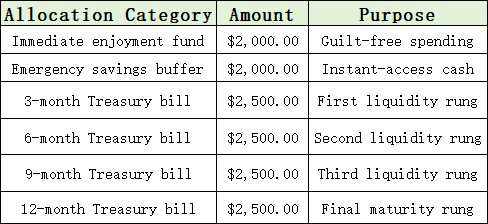

A practical example illustrates this clearly. Suppose a software engineer receives a $14,000 annual performance bonus. Historically, previous bonuses disappeared into dining, electronics, and spontaneous travel. This year, the engineer allocates the funds differently:

At the end of the year, most of the bonus still exists. More importantly, it has generated interest while remaining relatively accessible. Financial institutions note that laddering strategies reduce reinvestment timing risk because maturities are spread across intervals instead of concentrated into one date.

Another overlooked benefit is decision fatigue reduction. Large cash balances sitting in checking accounts silently invite repeated spending decisions. Bond ladders automate restraint. Once the ladder is established, the investor only needs to decide what to do when each rung matures.

Community discussions among Treasury ladder users reveal that many investors value the emotional stability of knowing cash becomes available regularly rather than remaining fully locked away. Several investors specifically mention that staggered maturities make emergency planning feel less stressful psychologically.

Practical Steps for Building Your Ladder

Step one is determining how much of your bonus to allocate. While some professionals may choose to invest the full amount, even partial deployment can improve financial outcomes. Decide whether to keep some cash on hand for immediate discretionary use while laddering the remainder.

Step two involves selecting suitable bonds. Short-term Treasury securities, municipal bonds, and highly-rated corporate notes are common options. Their durations are generally under 12 months, aligning perfectly with a laddering strategy for emergency liquidity.

Step three is execution. Break your bonus into equal slices and purchase bonds at the different maturity intervals. Using the example above, each $2,500 investment matures in a staggered pattern. This method ensures that within the next year, you will have access to funds four times, each time with accumulated interest.

Step four is monitoring. While short-term bonds are low-risk, keeping an eye on interest rates and reinvestment opportunities allows you to optimize returns without jeopardizing liquidity. Over time, as bonds mature, you can choose to roll them into new ladder rungs or redirect funds to other priorities, creating a rolling cycle of disciplined cash management.

Real-life data illustrates the power of this approach. According to a 2025 report from the Federal Reserve, short-term Treasury bills yielded an average of 4.8% over the year, outperforming standard savings accounts that averaged 1.2%. Even modest earnings like this can meaningfully augment your financial resilience, particularly when paired with an intentional spending plan.

Mistakes Professionals Make With Bonus Investing

Despite the simplicity of short-term ladders, several recurring mistakes reduce effectiveness.

The first is overextending maturities. Emergency liquidity should remain genuinely accessible. Stretching bonus money into five- or ten-year bonds exposes investors to greater interest-rate volatility and market pricing fluctuations. Most emergency-oriented ladders work best between three and twelve months.

The second mistake is ignoring inflation-adjusted outcomes. Some professionals focus solely on nominal yield percentages without considering real purchasing power. A 4% Treasury yield during a 5% inflation environment technically produces a negative real return. However, laddering still may outperform idle cash holdings losing purchasing power more rapidly.

The third mistake involves insufficient liquidity outside the ladder. Emergency funds should never become entirely dependent on future maturities. Many investors maintain one to three months of expenses in immediately accessible cash while laddering the remainder. Reddit discussions among Treasury ladder users repeatedly highlight the importance of maintaining a separate instant-access reserve for same-day emergencies.

The fourth mistake is operational neglect. Investors sometimes forget maturity dates, fail to reinvest proceeds, or accidentally allow cash to remain idle for weeks. One Treasury ladder discussion specifically mentioned reinvestment management becoming unexpectedly difficult without automation tools or reminders.

Automation solves much of this problem. Most brokerages now allow automatic Treasury reinvestment scheduling, reducing manual tracking requirements significantly.

(This article is intended for informational purposes only and should not be considered financial advice. Readers should consult a licensed financial advisor before making investment decisions.)

FAQs

Q1: Can I use bond ladders for smaller bonuses, like $500 or $1,000?

Yes, bond ladders work at any scale. The principle of staggered maturities applies equally to smaller amounts, although transaction fees may affect net returns for very small investments.

Q2: What if interest rates change during the ladder period?

Short-term bonds are less sensitive to interest rate fluctuations than long-term bonds. While rates may vary slightly, the impact on capital is minimal compared to potential gains from compound interest over the ladder period.

Q3: Are there risks to using corporate bonds in a ladder?

Yes, corporate bonds carry credit risk. Choosing high-rated corporations (AAA or AA) mitigates this risk, but Treasury and municipal bonds remain the safest options for short-term liquidity.

About Author

Evelyn Hartman is a financial strategist specializing in short-term investment solutions for professionals and freelancers. With over a decade of experience in wealth management, she focuses on practical strategies that blend capital preservation with modest growth.

References

[1] Federal Reserve. (2025). Treasury yields and short-term interest rates.

[2] Investopedia. (2024). How to build a bond ladder for short-term investments.

Make sure to explore the rest of this blog for more actionable strategies to turn financial windfalls into long-term stability.

Recommend:

Budget vs Expense Tracking: Understanding the Difference and Why You Need Both

Snowball vs Avalanche Method: Which Debt Repayment Strategy Works Best for You?

How to Turn Cashback Credit Cards Into Travel Rewards Without Falling Into Debt?

Protecting Your Investments from Inflation with TIPS and Floating-Rate Bonds