May 12, 2026

In this Article:

● Cashback credit cards can be a powerful tool for travel rewards if used strategically.

● Avoiding interest is critical to truly benefiting from rewards.

● Timing payments and aligning spending categories maximizes returns.

● Real-world examples show how travelers can earn hundreds in free flights annually.

● Maintaining financial discipline prevents debt traps while enjoying travel perks.

Estimated Reading Time: 12 minutes┃Post by: Harper Langston

Cashback Credit Cards and Travel Rewards

Cashback credit cards are often overlooked as travel tools, yet when optimized, they can unlock substantial travel rewards without resorting to high-interest debt. Many frequent travelers mistakenly believe that travel-specific cards are the only path to flights or hotel upgrades. However, strategic use of cashback cards can rival points-based programs if approached carefully.

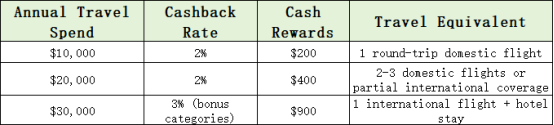

Consider Sarah, a freelance graphic designer who travels internationally four times per year. She uses a 2% cashback card on all travel-related expenses, including flights, accommodations, and dining. Over 12 months, her $20,000 in travel spending yields $400 in cash rewards. By converting these rewards into travel gift cards or airline credits through partner programs, she effectively reduces her travel costs without paying a cent in interest. The key is discipline: she pays her balance in full each month, ensuring the rewards aren’t offset by finance charges.

A simple table can illustrate the potential:

These figures are realistic for someone disciplined in both spending categories and timely payments.Building a “Travel Cashback System” Instead of Relying on One Card.

Many consumers assume the secret to maximizing travel rewards is finding a single “perfect” credit card. In reality, experienced travelers often use a layered system involving multiple cashback cards assigned to specific spending categories. The objective is not complexity for its own sake, but efficiency.

A common strategy in 2025 involves combining:

Under this structure, a traveler spending $3,500 monthly across categories could realistically generate between $900 and $1,500 annually in cashback value if balances are consistently paid in full.

Online communities focused on credit card optimization increasingly emphasize “ecosystem strategies,” where cashback earned from one card complements travel rewards from another. Reddit users tracking detailed yearly spending often report higher effective reward rates by pairing flat-rate cashback cards with travel-category cards instead of relying on premium luxury cards alone.

Another important trend is simplification. Many consumers initially open multiple premium cards only to realize they rarely use the associated benefits. Travelers are now prioritizing straightforward cashback structures that reduce mental overhead while still producing reliable rewards.

Why Interest Completely Destroys Reward Value

The mathematics behind credit card rewards are often misunderstood. Cashback percentages look attractive on marketing pages, but credit card APRs are dramatically higher than reward rates.

Consider this example:

This imbalance is why financially disciplined users benefit most from rewards programs. Recent reporting on rising U.S. credit card debt noted that banks increasingly rely on consumers who carry balances, while “transactors” — users who pay in full every month — extract the most value from reward systems.

Frequent travelers are particularly vulnerable because travel spending tends to be emotionally driven. Consumers often justify larger purchases by focusing on points or cashback rather than the actual expense. For example, a traveler might rationalize a $2,000 luxury hotel stay by emphasizing “earning 5x rewards,” despite creating a revolving balance that generates far more in interest charges than rewards earned.

Behavioral economists sometimes refer to this as “reward-induced overspending,” where consumers psychologically detach rewards from actual costs. The solution is operational discipline: treat the credit card strictly as a payment mechanism, not as additional income.

One effective approach used by financially disciplined travelers is the “pre-funded travel method.” Instead of charging vacations and figuring out repayment later, they first accumulate travel savings in a separate account. The credit card is then used purely for transaction efficiency and reward accumulation, while the cash already exists to immediately pay the balance.

Strategies to Maximize Rewards Without Interest

The first principle is simplicity: avoid revolving balances. Interest rates on credit cards often exceed 20%, and even the most generous cashback rewards can’t compete with compound interest charges. Align your card choices with your spending patterns. Cards offering 3–5% in bonus categories for travel, dining, or groceries can provide outsized rewards when timed correctly.

John, a marketing consultant, structures his spending around quarterly bonus categories. Q1 covers restaurants, Q2 for travel, and Q3 for online shopping. By tracking his expenses in a basic spreadsheet, he ensures all categories are fully utilized. He earns approximately $650 in annual rewards on $20,000 in spending.

Another real-world tactic is leveraging introductory bonuses. Many cashback cards offer $200–$500 rewards for spending $1,500–$3,000 in the first three months. By scheduling necessary travel expenses during this period, travelers can capture these bonuses without overspending. For instance, Emily booked her flights for an upcoming business trip using a new cashback card and met the minimum spend, earning a $300 bonus. This essentially covered the cost of one domestic flight.

Finally, monitoring reward redemption options is crucial. Some credit card issuers allow you to directly offset travel charges with cashback, while others convert rewards to points with partner airlines. Understanding the mechanics prevents value loss.

Common Pitfalls and Realistic Outcomes

Despite these strategies, travelers must recognize potential pitfalls. The most common mistake is treating cashback as “free money” and overspending. High-end restaurants, luxury hotels, or impulse trips financed on credit can erase any rewards gained.

Using a realistic scenario: Michael spends $25,000 annually on travel and lifestyle purchases. He earns 2% cashback, totaling $500. However, he carries an average balance of $3,000 at 20% APR. Interest costs alone consume roughly $600 per year, negating his rewards entirely. Avoiding this requires strict monthly payment discipline.

Another pitfall is neglecting card fees. Annual fees ranging from $95–$550 can reduce net benefits if not matched by sufficient rewards. For example, a $450 annual fee card offering 3% cashback on travel only makes sense if annual travel spending exceeds $15,000. Travelers must run the numbers before committing to premium cards.

Data from a 2025 consumer survey showed that disciplined cardholders who paid in full earned, on average, $450–$700 in travel-related cashback annually, while those who carried balances lost nearly $1,200 to interest. This stark contrast reinforces the importance of planning and payment discipline.

(This article is for informational and educational purposes only and should not be considered financial, legal, tax, or investment advice. Credit card rewards, cashback rates, annual fees, and promotional offers may change over time, so readers should verify details directly with financial institutions before making decisions. The examples and reward estimates in this article are illustrative and may not reflect actual results. The publisher and author are not responsible for financial losses, debt accumulation, or credit-related outcomes resulting from the use of the strategies discussed. Some content may include affiliate relationships, but all opinions remain independent and editorially unbiased.)

FQAs

Q1: Can I combine cashback rewards with airline miles?

Yes, many issuers allow converting cashback into travel points or gift cards. Check your card’s terms for conversion rates to ensure value is retained.

Q2: How do I avoid overspending while optimizing rewards?

Use a monthly budget and track spending categories. Only charge what you can pay off in full each month to prevent interest charges from negating rewards.

Q3: Are high-fee cards worth it for travel rewards?

Only if your spending aligns with bonus categories and expected rewards exceed the annual fee. Otherwise, low- or no-fee cards may provide better net benefits.

About Author

Harper Langston is a personal finance writer and travel-rewards researcher with over 10 years of experience covering credit card optimization, budgeting strategies, and consumer finance behavior. Her work focuses on helping readers maximize financial tools responsibly while avoiding common debt traps. Before becoming a full-time finance writer, Harper worked in consumer banking, analyzing credit usage patterns and reward-program trends. She is especially known for simplifying complex financial topics into practical, realistic strategies that everyday travelers and professionals can apply confidently.

References

[1] Chatzky, J. (2025). How to use cashback credit cards for travel rewards. NerdWallet.

[2] Brown, K. (2024). Avoiding interest traps on travel credit cards. The Points Guy.

[3] Smith, R. (2025). Credit card reward optimization strategies. Investopedia.

Maximizing travel rewards doesn’t have to be complicated—explore more strategies on our blog to turn everyday spending into unforgettable trips.

Recommend:

The Retirement Healthcare Strategy Most Americans Overlook: Maximizing Your HSA

Common Budgeting Mistakes and How to Avoid Them

How Low-Interest Personal Loans Can Simplify Your Finances Without Harming Your Credit

Smart Ways to Park a Work Bonus in Short-Term Bonds Without Losing Liquidity