May 15, 2026

In this Article:

● Many beginners underestimate their monthly expenses, leading to unrealistic budgets.

● Ignoring irregular expenses like car repairs or medical bills can disrupt your financial plan.

● Overly strict budgets can cause burnout and lead to overspending.

● Forgetting to adjust budgets over time limits financial growth and flexibility.

Estimated Reading Time: 12 minutes┃Post by: Alex Morgan

Budgeting is essential for financial health, but beginners often stumble into mistakes that make managing money more frustrating than freeing. Understanding common pitfalls and learning practical strategies to avoid them can help ensure that your budgeting efforts actually improve your financial life.

1. Underestimating Monthly Expenses

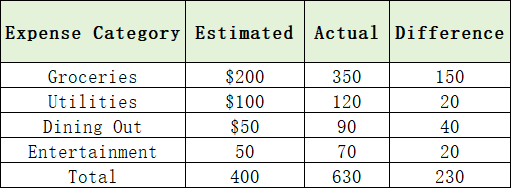

One of the most common errors is underestimating how much money you spend each month. Beginners often rely on rough guesses instead of tracking actual expenses. For example, you might assume your grocery bill is $200 per month, but after logging every purchase, you realize it’s closer to $350.

Example Table: Monthly Expense Misestimation

A gap of $230 might not seem huge, but over six months, that adds up to $1,380—money that could have been saved or invested.

Solution: Track all expenses for at least a month before setting your budget. Apps like Mint, YNAB, or even a simple spreadsheet can help identify your real spending habits.

2. Ignoring Irregular Expenses

Another frequent mistake is forgetting irregular or seasonal costs. These include car maintenance, medical bills, annual subscriptions, gifts, and taxes. Missing these can derail your monthly budget.

Scenario: Imagine you budget $50 per month for miscellaneous expenses but then need $300 for a car repair. Your tight monthly budget leaves you scrambling to cover the cost.

Practical Tip: Estimate irregular expenses and divide them by 12 to create a monthly allocation. This simple adjustment prevents surprises and keeps your budget realistic.

3. Creating an Overly Strict Budget

While discipline is important, overly rigid budgets often backfire. Restrictive limits on discretionary spending can make budgeting feel like a chore rather than a tool for empowerment, leading to frustration and eventual abandonment.

A balanced approach that includes planned flexibility allows for lifestyle adjustments without compromising financial goals. For example, allocating a portion of income for discretionary or lifestyle spending encourages adherence to the budget and promotes sustainable financial habits.

Better Approach: Include discretionary spending. Even $50 per month for personal treats can make sticking to a budget sustainable.

4. Failing to Track Actual Spending

Some beginners assume that creating a budget is enough—but without tracking spending, the plan is just a guess.

Consistent monitoring through apps or spreadsheets creates accountability and visibility. Recording daily expenditures and reviewing them weekly highlights overspending trends, which can then be addressed proactively. Tracking also fosters mindfulness, helping individuals make intentional choices rather than reactive purchases.

Strategy:

● Record every purchase for at least one month.

● Compare it with your budget weekly.

● Adjust allocations if certain categories consistently overshoot.

This not only identifies problem areas but also trains better spending habits.

5. Not Adjusting Your Budget Over Time

Budgets should evolve as your life changes. Static budgets are a common mistake. For example, your rent might increase, your income might rise, or you might start commuting more.

Regular review of the budget allows for timely adjustments in spending categories, savings targets, and investment contributions. Incorporating incremental increases in income or accounting for lifestyle changes ensures that the budget remains relevant and practical.

6. Overlooking Savings and Emergency Funds

Many beginners focus only on expenses and forget to prioritize savings. Without an emergency fund, unexpected costs force you to borrow or use credit cards, defeating the purpose of budgeting.

Establishing a minimum savings target each month encourages financial resilience. A systematic approach to building emergency funds, retirement contributions, and long-term investments creates stability and ensures that financial setbacks do not derail overall plans. Consistent saving also instills discipline and encourages a long-term mindset.

Guideline: Aim to save at least 10–20% of your income monthly. If income is $2,500, allocate $250–$500 to savings. Even small amounts compound over time:

● Saving $300 per month at 5% annual interest grows to ~$3,700 in one year.

● Over 5 years, it can exceed $20,000 with compound interest.

7. Overlooking Financial Goals

Many beginners focus solely on covering monthly expenses and fail to align their budget with short-term and long-term financial goals. Without clearly defined goals, budgets often become reactive rather than proactive, and money is spent without purpose.

Setting specific financial goals—such as paying off a student loan within two years, saving for a down payment, or building a six-month emergency fund—provides direction. Each goal should have a target amount, a timeline, and a monthly contribution plan, which ensures that budgeting decisions consistently support progress.

8. Neglecting Debt Management

A budget that ignores existing debt obligations can create financial strain. High-interest debt, such as credit cards or personal loans, can consume a significant portion of income if not accounted for, undermining savings and investment plans.

Including debt repayment as a formal category in your budget ensures that obligations are met systematically. Strategies like the snowball or avalanche method can be paired with budgeting to accelerate debt reduction and minimize interest costs. Prioritizing high-interest debt first often saves the most money over time.

9. Not Reviewing Subscriptions and Recurring Payments

Automatic subscriptions are often overlooked in budgets, quietly draining funds each month. Over time, small recurring payments can accumulate into a significant expense.

Conducting a quarterly audit of all recurring payments—streaming services, software subscriptions, gym memberships—can reveal unnecessary expenses. Cancelling or downgrading unused or underused services frees up money that can be redirected toward savings or debt repayment.

(The content of this article is intended for educational purposes only and should not be considered financial advice. Readers are encouraged to consult a certified financial advisor before making significant financial decisions.)

FAQs

Q1: How long should I track expenses before creating a budget?

A: At least one month is recommended to capture both regular and irregular spending.

Q2: What is the best method for beginners to track spending?

A: Simple spreadsheets or budgeting apps like Mint or YNAB work well for most beginners.

Q3: How do I avoid feeling restricted by my budget?

A: Allocate a small, flexible amount for discretionary spending to maintain motivation and avoid burnout.

About Author

Alex Morgan is a certified personal finance educator with over 10 years of experience helping beginners master budgeting and financial planning. He specializes in practical, real-world strategies for everyday money management.

References

[1] Investopedia. (2024). Budgeting mistakes to avoid.

[2] NerdWallet. (2023). How to track your spending.

[3] The Balance. (2024). Creating a flexible budget for beginners.

Stay on this blog to explore more practical personal finance tips that can transform your financial habits today!

Recommend:

Frugal Living for Beginners: Practical Steps to Save Money and Live Well

Why Your Paycheck Disappears Before Rent?

How to Turn Cashback Credit Cards Into Travel Rewards Without Falling Into Debt?

Budgeting with Irregular Income: A Practical Guide for Beginners