May 16, 2026

Hidden payroll deductions can quietly shrink your paycheck, but by reviewing pay stubs and managing benefits wisely, you can take control of your take-home pay and avoid the “disappearing paycheck” trap.

Estimated Reading Time: 11 minutes┃Post by: Sarah Mitchell

It’s a familiar frustration: you receive your paycheck, glance at the number, and feel a rush of excitement—only for that feeling to evaporate when you tally your bills. Rent, utilities, groceries, and transportation seem to consume every dollar, leaving little room for discretionary spending. While it’s easy to blame overspending, the reality is that many employees don’t see the full picture of their take-home pay. Hidden deductions and employer contributions can quietly reduce what lands in your account, often before you even realize it.

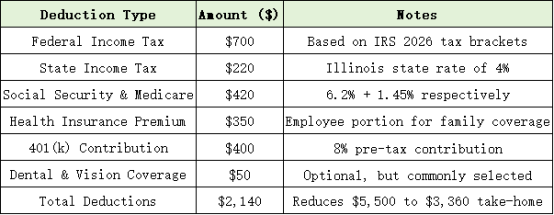

Take, for example, a software engineer in Chicago earning $5,500 monthly before taxes. At first glance, $5,500 seems like a comfortable income, enough to cover rent, student loans, and daily expenses. Yet, after factoring in taxes, health premiums, retirement contributions, and other deductions, the actual take-home may be closer to $3,900—a discrepancy that shocks many new workers.

Understanding Hidden Deductions

Some deductions are obvious: federal, state, and Social Security taxes. Others, however, fly under the radar. Health insurance premiums, dental and vision coverage, life insurance, and accidental disability insurance all subtract from your paycheck. Additionally, employer-sponsored retirement plans can impact take-home pay, especially if contributions are automatically withheld or mismatched.

Consider the following illustrative table of deductions for our hypothetical software engineer:

This table demonstrates that even with a seemingly high gross income, deductions can slash take-home pay by nearly 40%. Many workers are unaware of the cumulative effect until they analyze their pay stubs in detail.

Real-Life Scenarios

Imagine Maria, a young marketing professional living in New York City. Her gross monthly income is $4,800. She contributes 5% of her salary to a 401(k), pays $280 for health coverage, and has a pre-tax commuter benefit of $120. By the time she receives her paycheck, she’s left with $3,450—barely enough to cover her $1,700 rent, student loans, and groceries.

Similarly, John, a mid-level engineer in Seattle, was surprised to find his take-home pay was $1,000 less than expected. The culprit? His employer had auto-enrolled him in the company’s supplemental life insurance plan and increased his 401(k) match contribution without a clear notice. Many employees aren’t proactive in checking these automatic deductions, assuming that what they see on their contract or offer letter is what they’ll receive.

The Impact of Employer Contributions

Many workplace deductions are partially or fully matched by employers. While this is a benefit, it can create confusion. For example, if an employee contributes 5% to a 401(k), the employer may match up to 3%. While the match doesn’t reduce take-home pay, understanding the total contribution is crucial for long-term financial planning. In some cases, employees may feel their paycheck is smaller than expected because they’re not factoring in voluntary deductions like health savings accounts (HSAs) or flexible spending accounts (FSAs).

Breaking Down Payroll Statements

One of the most effective ways to understand paycheck reductions is to review the detailed payroll statement each month. Look for entries under “pre-tax” and “post-tax” deductions. Pre-tax deductions reduce taxable income, which can save money in taxes but reduce immediate cash flow. Post-tax deductions, such as certain insurance premiums or wage garnishments, directly reduce take-home pay.

A visual example:

Gross Pay: $5,500

Pre-Tax Deductions: $850

Taxable Income: $4,650

Taxes Withheld: $1,350

Post-Tax Deductions: $400

Net Pay: $2,900

By breaking it down step by step, employees can identify areas where small changes could have a big impact. For instance, adjusting retirement contributions or reviewing optional insurance plans can free up hundreds of dollars per month.

Strategies to Manage Hidden Deductions

While you cannot eliminate mandatory deductions, several strategies help employees maximize their take-home pay:

Audit Your Benefits: Review health, dental, and vision coverage annually to ensure you’re not overpaying for unnecessary plans.

Adjust 401(k) Contributions: While contributing to retirement is essential, adjusting contributions can temporarily increase take-home pay if needed.

Explore Pre-Tax Accounts: Utilize FSAs or HSAs strategically to reduce taxable income without sacrificing essential coverage.

Regular Pay Stub Review: Understanding each line item helps catch unexpected deductions early.

A recent survey by the Employee Benefit Research Institute revealed that 42% of employees underestimate their total payroll deductions by at least 20%. Moreover, 35% admitted they rarely check their pay stubs, highlighting a widespread gap in financial awareness.

Another study by PwC found that employees who actively review their deductions and adjust optional benefits save an average of $1,200 annually, demonstrating the tangible value of awareness and proactive management.

Hidden payroll deductions are a silent drain on many workers’ finances. While gross income may appear sufficient, the reality of pre- and post-tax deductions can dramatically reduce take-home pay. By understanding these deductions, reviewing pay stubs, and strategically managing benefits, employees can regain control over their finances and avoid the common “paycheck disappears before rent” scenario.

(This article is for informational purposes only and is not financial, legal, or tax advice. Individual circumstances vary, so consult a licensed professional before making decisions about paycheck management, benefit enrollment, or retirement contributions. The author and blog are not responsible for any financial outcomes from applying this content.)

FQAs:

Q1: Can I opt out of employer-sponsored benefits to increase my take-home pay?

Some benefits are optional, such as supplemental insurance plans. However, mandatory deductions like taxes and Social Security cannot be avoided.

Q2: How often should I review my paycheck for deductions?

Monthly reviews are recommended to catch errors and understand how pre-tax and post-tax deductions affect take-home pay.

Q3: Are automatic 401(k) contributions reversible?

Yes, most plans allow you to adjust contribution percentages at least once per quarter, sometimes more frequently.

About Author

Sarah Mitchell is a personal finance writer and former payroll consultant with over 12 years of experience helping employees understand paychecks, benefits, and retirement contributions. She simplifies complex financial concepts with real-world examples, empowering readers to make informed decisions. Outside of finance, Sarah enjoys budget-friendly cooking, urban hikes, and teaching financial literacy in her community.

References

[1] Employee Benefit Research Institute. (2025). Payroll awareness and deduction trends.

[2] PwC. (2024). Employee financial wellness survey.

[3] U.S. Internal Revenue Service. (2026). Understanding payroll deductions.

Stay tuned to our blog for more practical tips that help you take control of your daily finances and avoid common money traps.

Recommend:

The Realistic Timeline to Becoming Debt-Free: Step-by-Step Guide for Beginners

How to Build Financial Security on a Low Income?

How to Create a Budget for Beginners?

How Robo-Advisors Can Build an ESG Micro-Portfolio Focused on Emerging Markets