May 17, 2026

Key Takeaways:

● Budgeting starts with knowing exactly how much money you earn each month.

● Tracking every expense helps you see where money leaks occur.

● Categorizing expenses into needs, wants, and savings clarifies priorities.

● A monthly budget helps balance daily spending with long-term financial goals.

● Consistently reviewing and adjusting your budget ensures long-term success.

Estimated Reading Time: 15 minutes┃Post by: Emma Caldwell

Creating a budget for beginners means setting up a realistic plan for your money that helps you control spending, save for the future, and avoid unnecessary debt. Budgeting is not about restricting yourself—it’s about gaining clarity and confidence in how your money flows. For beginners, the key is to make the process simple, actionable, and realistic, rather than overwhelming.

Step-by-Step Tutorial

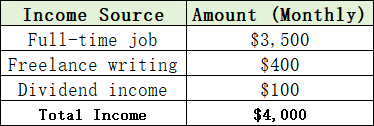

Step 1: Calculate Your Total Income

The first step in budgeting is knowing exactly how much money comes in each month. Include your full-time salary, part-time work, freelance earnings, bonuses, or passive income like dividends or rental income. If your income fluctuates, use an average over the past 6–12 months to create a conservative baseline.

Example Monthly Income:

Knowing your total income sets the upper limit for your spending and helps determine how much you can realistically allocate to savings.

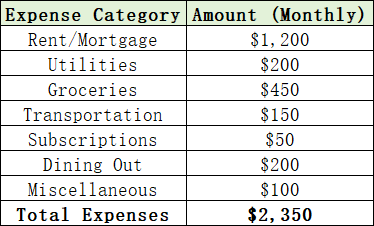

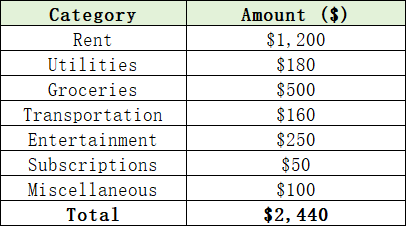

Step 2: Track Your Expenses

Next, track every expense for at least one month. Many beginners underestimate how small, frequent purchases add up. Use apps, spreadsheets, or simply a notebook. Include everything: rent, utilities, groceries, transportation, subscriptions, dining out, and irregular expenses like gifts or car repairs.

Example Monthly Expenses:

Tracking your expenses helps reveal “money leaks,” areas where you spend without realizing, and patterns that might need adjustment.

Step 3: Categorize Your Spending

To simplify your budget, divide your expenses into three main categories: needs, wants, and savings.

Needs: Essentials like rent, utilities, groceries, transportation, and insurance.

Wants: Non-essential spending, such as entertainment, dining out, hobbies, and travel.

Savings: Contributions to an emergency fund, retirement accounts, or investments.

Example Categorization:

This breakdown allows you to see if you are living within your means, overspending on wants, or neglecting savings.

Step 4: Set Financial Goals

Financial goals give your budget purpose and focus. Start with short-term goals (0–12 months) and long-term goals (1–10 years).

Short-term goals:

● Pay off $1,000 credit card debt in 6 months

● Build a $500 emergency fund

● Save for a vacation

Long-term goals:

● Save for a house down payment

● Contribute consistently to retirement accounts

● Build an investment portfolio

Use the SMART method: Specific, Measurable, Achievable, Relevant, and Time-bound. Goals make it easier to allocate money consistently and track progress.

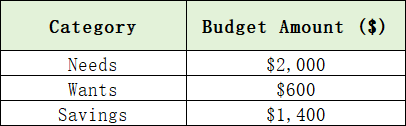

Step 5: Create a Monthly Budget

Using the income and expense data, create a realistic monthly budget. One popular framework is the 50/30/20 rule:

● 50% for needs

● 30% for wants

● 20% for savings

Adjust percentages based on your financial situation. For beginners, the key is flexibility. Avoid strict rules that feel impossible; a practical, slightly imperfect budget is better than no budget at all.

Sample Budget Using 50/30/20 Rule:

Step 6: Monitor and Adjust Your Budget

A budget is not a static plan. Life changes—income may rise or fall, bills increase, and new goals emerge. Review your budget monthly and adjust accordingly.

Tips for Monitoring:

● Use apps like Mint, YNAB, or Personal Capital to track automatically.

● Review bank statements weekly.

● Adjust discretionary spending before dipping into savings.

● Celebrate milestones to stay motivated.

Hypothetical Case Study: Jane’s Budget Journey

Scenario:

Jane is 28, works in marketing, and earns $4,000 per month. Despite trying to save, she often ends up overspending on entertainment.

Step 1: Income

Jane totals $4,000 from her salary.

Step 2: Expenses Tracking (First Month)

Jane sees she spends $250 on entertainment—more than she needs.

Step 3: Categorization

She reallocates $150 from entertainment to her emergency fund, giving her a realistic saving plan.

Step 4: Budget Plan

Needs: $2,040

Wants: $400

Savings: $1,560

Step 5: Outcome

After three months, Jane has saved nearly $4,680 and gained control over her discretionary spending. She feels confident about her money and even starts planning for a small vacation using a portion of her “wants” category without harming her savings.

Advanced Budgeting Tips for Beginners

1. Automate Savings

Set up automatic transfers to savings or investment accounts right after payday. This reduces the temptation to spend what you plan to save.

2. Include Irregular Expenses

Car repairs, medical bills, and annual subscriptions can derail a budget if unplanned. Allocate a small monthly amount to cover these.

3. Use Cash for Certain Categories

For discretionary spending (dining out, entertainment), consider using cash. This creates a natural spending limit.

4. Track Your Progress

Keep a monthly journal or spreadsheet to record successes and setbacks. Reviewing progress reinforces positive habits.

5. Adjust for Lifestyle Changes

Moving cities, changing jobs, or starting a family requires adjusting your budget. Flexibility ensures your financial plan remains realistic.

(The content provided is for educational purposes only and should not be considered professional financial advice. Readers are encouraged to consult a certified financial advisor for guidance specific to their circumstances.)

FAQs

Q1: What if my income fluctuates monthly?

Track your average income over the past 6–12 months and base your budget on the lower end to avoid overspending. Adjust savings and discretionary spending when income exceeds expectations.

Q2: Can I budget without tracking every small expense?

Yes, but tracking even a few key categories can reveal spending patterns. Major categories like groceries, bills, and dining out usually account for most discretionary spending.

Q3: How much should I allocate to savings as a beginner?

A common recommendation is at least 20% of monthly income, but beginners may start with 10% and gradually increase as they get comfortable with budgeting.

About Author

Emma Caldwell is a personal finance coach with over 8 years of experience helping young professionals manage money, reduce debt, and build wealth. She specializes in making budgeting simple, actionable, and sustainable for beginners.

References

[1] Investopedia. (2023). Budgeting basics.

[2] NerdWallet. (2023). How to create a budget.

Recommend:

Smart Moves: Exercising Employer Stock Options During Market Downturns Without Paying Excess Taxes

Budgeting with Irregular Income: A Practical Guide for Beginners

How Long It Really Takes to Build Your Credit?

How Freelancers Can Avoid Hidden FX Fees When Getting Paid Internationally