May 13, 2026

Key Points:

● Building a credit history takes at least 6 months, but meaningful scores often require 1–3 years.

● On-time payments and low credit utilization are the foundation of a strong credit score.

● Beginners can use secured credit cards, credit-builder loans, or authorized user accounts to start safely.

● Responsible credit behavior over time pays off; mistakes can significantly delay progress.

● Tracking, monitoring, and understanding your credit profile is essential for long-term financial health.

Estimated Reading Time: 18 minutes┃Post by: Jamie Rivers

Building credit is a gradual process that depends on consistent responsible behavior. For a person starting from scratch, it typically takes 6 months for any credit activity to appear on your credit report. By this point, you’ll have a basic credit score, though it’s often in the 300–600 range. Reaching a strong, mainstream credit score (around 650–700) usually requires 1–3 years, depending on how you manage your accounts.

Key factors affecting your timeline include:

Payment history: Paying bills late is the biggest score killer.

Credit utilization: How much of your available credit you actually use.

Account age: Older accounts improve your score over time.

Credit mix: Revolving accounts (like credit cards) and installment loans (like car or student loans) together are ideal.

By understanding how each factor influences your credit, you can accelerate progress while avoiding common mistakes that set beginners back.

Step-by-Step Tutorial

Here’s a realistic, actionable plan to build credit from zero:

Step 1: Check Your Starting Point

Even if you have no credit, start by requesting your free annual credit report from AnnualCreditReport.com.

Verify your identity, check for errors, and confirm you have no negative items that might already exist due to identity theft or clerical mistakes.

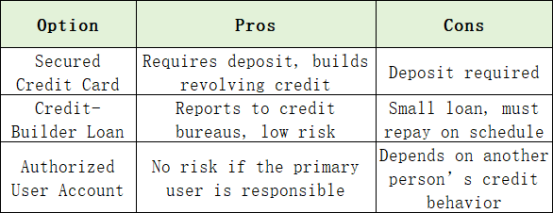

Step 2: Choose the Right First Credit Account

For beginners, low-risk accounts are ideal:

Step 3: Use Credit Responsibly

Using credit responsibly is the cornerstone of building a strong credit profile. One of the most important habits is keeping your credit utilization low, ideally under 30% of your available credit. For example, if your card has a $500 limit, try to carry no more than $150 at any time. Paying your full balance on time each month is equally crucial. Even one late payment can significantly damage your score and set back months of progress. Think of each payment as a building block: consistency over time creates a stable foundation for your credit history.

Step 4: Diversify Your Credit Mix

Once you have a few months of credit history, it’s beneficial to diversify the types of credit you use. Lenders and scoring models like to see a mix of revolving credit, such as credit cards, and installment loans, like a small personal or student loan. This demonstrates that you can handle different types of financial obligations responsibly.

For beginners, starting with one secured card and then adding a credit-builder loan or a retail store card after 6–12 months is often a safe approach. Keep in mind, though, that opening multiple accounts at the same time can hurt your score temporarily due to hard inquiries, so spacing applications is important.

Step 5: Monitor Your Progress

Tracking your progress regularly helps you stay on top of your credit-building journey and catch potential issues early. Free tools like Credit Karma, Experian, or Mint allow you to monitor your score, check your credit utilization, and receive alerts for any new inquiries or changes in your credit profile. Reviewing your accounts monthly gives you insight into patterns, such as consistently high utilization or missed payments, and allows you to adjust habits proactively. Seeing the steady improvement in your score can also motivate you to maintain responsible credit behavior over the long term.

Step 6: Avoid Common Pitfalls

Building credit requires vigilance because certain mistakes can derail months of progress. Avoid maxing out your credit cards, even temporarily, as high utilization can negatively impact your score. Don’t close old accounts too soon; the length of your credit history is an important factor in your score. And resist the temptation to apply for multiple credit cards or loans in a short period, as each hard inquiry can lower your score slightly. Even one late payment can erase weeks of careful progress, so consider setting up automatic payments or reminders to protect against human error.

Step 7: Plan for Long-Term Credit Health

Credit-building is a long-term strategy, not a quick fix. As your score improves, start planning for future financial goals, such as qualifying for a personal loan, auto loan, or even a mortgage. Gradually increasing your credit limit, maintaining low utilization, and continuing timely payments will help you sustain a strong credit profile. Additionally, periodically reassessing your credit habits ensures you are not falling into bad practices, such as overspending or ignoring account activity. Long-term planning combined with consistent, responsible behavior sets the stage for not only a high credit score but also greater financial security and access to better financial products.

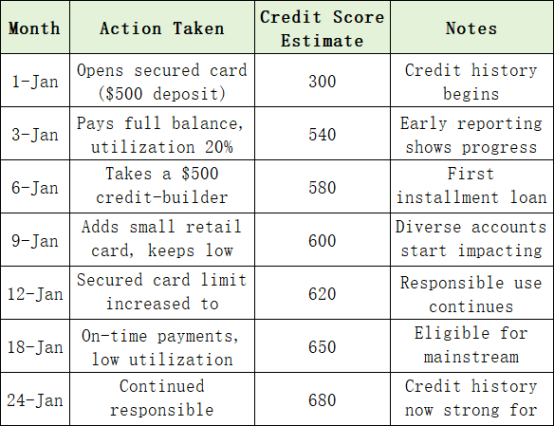

Hypothetical Case Study

Let’s follow Alex, 22, who starts with no credit:

Note: Consistency is more important than rapid changes. Even small accounts matter if managed correctly. Credit-building is a marathon, not a sprint.

Tools: Apps/Templates

Apps for Tracking and Alerts:

· Credit Karma: Weekly updates, credit monitoring, and alerts for inquiries.

· Experian: Real-time FICO score updates, identity theft monitoring.

· Mint: Budget tracking, reminders for credit payments, and utilization monitoring.

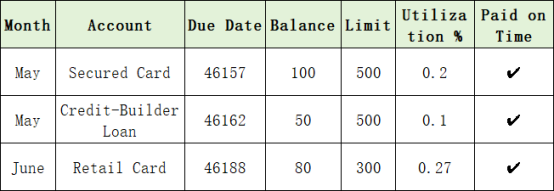

Templates for Beginners:

This makes credit-building visible, measurable, and actionable, helping beginners stay consistent.

Payment Reminder Calendar:

· Google Calendar or phone reminders to pay bills before the due date.

· Even a two-day buffer prevents accidental late payments.

Tips to Accelerate Credit Growth

Become an Authorized User: Being added to a responsible family member’s card can instantly establish history.

Keep Utilization Low: Even if you have the funds to spend, using only 10–20% of available credit signals financial responsibility.

Make Small, Regular Purchases: Avoid zero activity; some credit use is needed for scoring.

Automate Payments: Avoiding late payments is easier with autopay.

Review Reports Regularly: Catch errors early; disputes can restore lost points quickly.

(This article provides general financial education and is not financial, legal, or credit advice. Individual experiences may vary, and readers should consult a professional for personal guidance.)

FAQs

Q1: Can I build credit without a credit card?

Yes. Credit-builder loans or installment loans from a credit union can help establish credit history.

Q2: How long before my credit score reaches 700?

Typically 2–3 years of responsible use, depending on account type, utilization, and payment history.

Q3: Will checking my own credit hurt my score?

No. Soft inquiries (like personal credit checks) do not affect your score.

About Author

Jamie Rivers is a certified personal finance coach who specializes in guiding beginners through credit-building, budgeting, and responsible borrowing. Jamie has helped hundreds of young adults achieve financial milestones safely, from opening their first credit card to qualifying for their first mortgage.

References

[1] Experian. (2026). How long does it take to build credit?

[2] AnnualCreditReport.com. (2026). Get your free credit report.

[3] Credit Karma. (2026). Credit score and report insights.

Stay consistent and explore more beginner-friendly strategies on our blog to strengthen your financial health over time.

Recommend:

Budget vs Expense Tracking: Understanding the Difference and Why You Need Both

Smart Moves: Exercising Employer Stock Options During Market Downturns Without Paying Excess Taxes

How to Improve Your Credit Score?

The Gig Worker’s Guide to Lowering Estimated Taxes With Investment Losses