May 14, 2026

Key Takeaways:

● Gig workers often face fluctuating income, making quarterly estimated taxes tricky.

● Tax-loss harvesting can strategically offset gains and reduce taxable income.

● Selling underperforming investments before year-end may lower tax liability.

● Combining tax-loss harvesting with careful income tracking helps optimize cash flow.

Estimated Reading Time: 12 minutes┃Post by: Jamie Lowell

Tax-Loss Harvesting for Gig Workers

For freelancers, independent contractors, and side-hustlers, income can swing dramatically month to month. Unlike salaried employees with predictable withholding, gig workers must estimate and remit quarterly taxes, often leading to overpayments or unexpected bills. Tax-loss harvesting offers a strategic approach to this challenge. Essentially, it involves selling investments that have decreased in value to realize a capital loss. That loss can then offset other taxable income, including capital gains and potentially some ordinary income, thereby reducing the overall tax burden.

Consider a graphic illustration:

In this scenario, the $2,000 loss from Stock A can offset the $1,500 gain from Stock B, leaving a $500 net capital loss. Depending on the tax code, this $500 may further reduce ordinary income for the year. For gig workers, applying this approach before quarterly estimated taxes are due can make a meaningful difference in cash flow management.

Realistically, many freelancers keep a small portfolio or invest in mutual funds or ETFs. Tax-loss harvesting isn’t limited to individual stocks—it works across most taxable investment accounts. The key is timing: losses need to be realized within the tax year and not repurchased within 30 days to avoid the wash-sale rule.

Practical Implementation for Quarterly Tax Planning

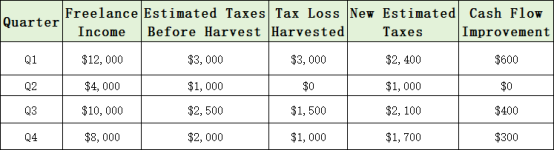

Let’s walk through an example. Alex, a freelance graphic designer, has a highly variable income. Q1 brought in $12,000, but Q2 is projected at only $4,000. Alex also holds several stocks with unrealized losses. By selling certain investments with a $3,000 cumulative loss in late Q1, Alex offsets part of the income spike, reducing Q1 estimated taxes from $3,000 to $2,400. This $600 cash saving allows Alex to reinvest in the business or cover living expenses.

An illustrative table demonstrates the potential savings across four quarters:

From this example, it’s clear that careful integration of tax-loss harvesting can smooth the burden of quarterly estimated taxes. Beyond numbers, it’s also a matter of planning. Maintaining a calendar of projected income and potential investment losses helps gig workers make timely decisions.

It’s important to note that tax-loss harvesting does not create new income—it simply defers or offsets taxes. Over time, disciplined application can improve overall financial efficiency. Freelancers who incorporate this strategy often find more predictable cash flow, reducing the stress of large tax payments at the end of the quarter or year.

Carrying Forward Losses Into Future Tax Years

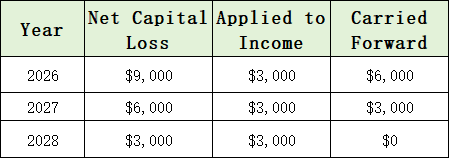

Tax-loss harvesting can remain useful even when losses exceed current-year gains. According to IRS guidance and financial planning resources, unused capital losses can carry forward indefinitely into future tax years. Up to $3,000 of excess losses may also offset ordinary income annually.

For gig workers with volatile income, this feature creates flexibility. Imagine a freelance web developer experiencing a weak market year with substantial investment losses but limited taxable income. Instead of “wasting” those losses, they can preserve them for future years when business income rebounds significantly.

This long-term aspect makes tax-loss harvesting more strategic than many freelancers initially realize.

The Psychological Side of Freelance Tax Planning

Taxes create unusual financial stress for freelancers because income arrives without automatic withholding. Unlike salaried employees, gig workers must continuously reserve money for future tax obligations while also covering business expenses and personal living costs. Recent reporting has shown estimated-tax penalties increasing substantially among self-employed taxpayers and investors due to fluctuating income and poor planning.

Tax-loss harvesting can indirectly improve financial confidence by giving freelancers a greater sense of control over unpredictable tax obligations. Even modest reductions in estimated payments may improve short-term liquidity during slower business periods. Many experienced independent contractors eventually treat taxes like an ongoing monthly operating expense rather than a once-a-year emergency.

Real-World Considerations and Risks

While the concept is straightforward, several real-world factors influence effectiveness. Market volatility means that losses are not guaranteed; investments may recover before realizing a tax benefit. Additionally, careful record-keeping is essential to comply with IRS rules, especially the wash-sale rule, which disallows the deduction if a substantially identical investment is repurchased within 30 days.

Gig workers should also weigh transaction costs. Frequent buying and selling may incur brokerage fees that partially offset tax savings. In many cases, using ETFs or low-cost mutual funds can minimize these costs while still enabling strategic harvesting.

Another practical consideration is integrating tax-loss harvesting with overall financial planning. For example, freelancers might combine this strategy with retirement contributions, health savings accounts, and deductible business expenses. This multi-layered approach can amplify tax efficiency and optimize quarterly cash flow.

Lastly, it’s wise to consult with a tax professional. While self-directed software tools help, individual circumstances vary, and small missteps can have outsized effects. A CPA or financial advisor familiar with freelance tax scenarios can provide guidance tailored to income volatility and investment behavior.

(This article is for educational purposes only and should not be considered financial, tax, or investment advice. Tax laws and investment regulations can change, and individual financial situations vary significantly. Readers should consult a licensed CPA, tax professional, or financial advisor before making decisions related to tax-loss harvesting or estimated taxes. Investing involves risk, including possible loss of principal, and the author and publisher are not responsible for financial outcomes resulting from the use of this content. Finance blogs commonly use disclaimers to clarify that content is informational rather than personalized advice.)

FQAs

1. Can I use tax-loss harvesting for cryptocurrency investments?

Yes, tax-loss harvesting applies to most taxable investments, including cryptocurrencies, as long as transactions are executed in a taxable account and adhere to the IRS rules.

2. What happens if I buy the same stock immediately after selling it for a loss?

This triggers the wash-sale rule, which disallows the loss deduction. You must wait at least 31 days before repurchasing the same or substantially identical security.

3. Does tax-loss harvesting reduce my total tax bill for the year?

It can lower taxable income, potentially reducing your overall tax liability, but the total benefit depends on your gains, losses, and income bracket.

About Author

Jamie Lowell is a fictional Certified Financial Planner (CFP®) and freelance finance writer specializing in tax strategies for gig workers, freelancers, and self-employed professionals. With more than 10 years of experience covering personal finance and independent contractor taxation, Jamie focuses on simplifying complex financial concepts into practical, real-world strategies readers can apply immediately. Jamie’s work frequently explores quarterly tax planning, freelance cash-flow management, tax-efficient investing, and financial systems for irregular-income households.

References

[1] Internal Revenue Service. (2024). Topic No. 409 Capital Gains and Losses.

[2] IRS. (2024). Estimated Taxes.

[3] Morningstar. (2024). Tax-Loss Harvesting Strategies.

Explore more insightful articles here to stay ahead in managing your freelance finances efficiently!

Recommend:

The Retirement Healthcare Strategy Most Americans Overlook: Maximizing Your HSA

Budget vs Expense Tracking: Understanding the Difference and Why You Need Both

How to Improve Your Credit Score?

How Low-Interest Personal Loans Can Simplify Your Finances Without Harming Your Credit