May 14, 2026

Key Highlights:

● Combining budgeting and expense tracking improves financial awareness.

● Expense tracking can reveal hidden spending habits.

● Budgets help prioritize savings and debt repayment.

● Realistic finances require both planning and monitoring.

Estimated Reading Time: 12 minutes┃Post by: Jordan Maxwell

When it comes to managing money, the terms budgeting and expense tracking are often used interchangeably—but they are not the same. A budget is your financial roadmap, a plan for how you intend to use your money over a certain period. Expense tracking, on the other hand, is the process of monitoring and recording the money you actually spend. Both are essential for financial health, yet they serve distinct purposes.

The Role of Budgeting

Budgeting is proactive. It requires you to sit down, assess your income, list your obligations, and allocate funds to various categories—rent, utilities, groceries, entertainment, and savings. Think of a budget as a map that helps you navigate the month. For instance, if your monthly income is $3,000, your budget might allocate $1,000 to rent, $500 to food, $300 to transportation, and $400 to savings. A well-constructed budget ensures that your spending aligns with your financial goals.

The realism of budgeting comes into play when you adapt your plan to your lifestyle. Some people try to create an “ideal” budget that’s overly strict. For example, cutting coffee from $100 per month to $0 might sound like an easy savings hack—but if it’s not realistic, you’re less likely to stick to the plan. Realistic budgeting acknowledges small indulgences while prioritizing essentials and savings.

The Role of Expense Tracking

Expense tracking is reactive but equally important. It answers the question, “Where did my money actually go?” Tracking expenses can be as simple as using a notebook, a spreadsheet, or apps like Mint, YNAB (You Need a Budget), or PocketGuard.

By recording each purchase, you create a mirror for your spending habits. Maybe you budgeted $200 for dining out, but tracking reveals you spent $350. This awareness allows you to adjust your future budget or change habits. Expense tracking also helps uncover patterns, such as recurring subscription services that go unnoticed until you see them listed month after month.

Why You Can’t Have One Without the Other

Using just a budget without tracking can be like navigating with a map but never checking if you’re on the right road. Conversely, tracking expenses without a budget is like keeping a diary without a goal—you know what you spent, but you don’t know if it aligns with your priorities.

Imagine a real-life scenario: Sarah earns $4,000 per month and budgets $500 for groceries. She diligently tracks every dollar and discovers she consistently spends $650. Without tracking, she might never notice, and overspending in one area could derail her savings or debt repayment plan. With both budgeting and tracking, she can adjust her grocery budget, plan for occasional treats, and still meet her financial goals.

Practical Tips for Balancing Budgeting and Expense Tracking

1. Start Simple: Don’t overcomplicate your budget. List core categories like housing, food, transportation, and savings first.

2. Automate Tracking: Link your bank accounts to tracking apps. Automation reduces the likelihood of missed expenses.

3. Set Realistic Goals: Overly strict budgets often fail. Allow some flexibility for lifestyle choices.

4. Review Weekly: A quick weekly review of expenses helps spot discrepancies before they grow into problems.

5. Adjust Gradually: Budgets are not static. Modify categories based on actual spending trends.

Budgeting and tracking also affect behavior. Seeing your spending in black and white can encourage mindful purchases. For instance, knowing you’ve spent $300 on coffee in a month may prompt you to brew at home more often. Meanwhile, a well-planned budget can create a sense of control, reducing financial anxiety.

Tools: Apps and Templates

Apps for Budgeting

1. YNAB (You Need A Budget): Focuses on zero-based budgeting.

2. Mint: Offers automated tracking and budget suggestions.

3. PocketGuard: Simplifies daily spending monitoring.

Templates

● Excel/Google Sheets: Customizable for monthly budgets and tracking.

● Printable Budget Planners: Useful for those who prefer pen and paper.

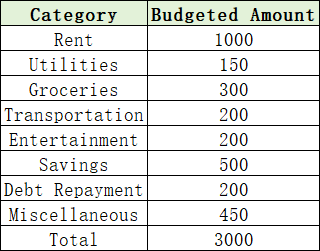

Hypothetical Case Study: Emily’s Monthly Finances

Scenario:

Emily earns $3,000 per month and wants to save $500, pay off $200 in credit card debt, and still enjoy her lifestyle.

Budget:

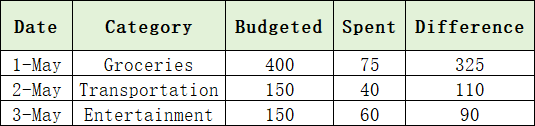

Expense Tracking Results:

Emily tracked her spending for the month: she overspent $100 on dining out but saved $50 on transportation.

Analysis:

● Her savings goal remained intact, but entertainment needed adjustment.

● She decided to reduce dining out by $50 and entertainment by $50 to balance the budget.

Key Takeaway: Tracking revealed overspending patterns, allowing Emily to tweak her plan without compromising her financial goals.

Common Mistakes to Avoid

● Not tracking small purchases: Coffee runs, app subscriptions, and snacks add up.

● Ignoring irregular expenses: Annual insurance payments or gifts can disrupt a monthly budget if unplanned.

● Being too rigid: Life is unpredictable. Budget flexibility is crucial.

● Relying solely on digital tools: Apps help, but occasionally reviewing receipts manually ensures accuracy.

Think of budgeting and expense tracking as a two-step process. Budgeting answers the question, “What should I do with my money?” Expense tracking answers, “What did I actually do with my money?” Together, they give a realistic, actionable picture of your finances. Over time, combining these practices helps you save more, spend wisely, and make informed financial decisions.

Even seasoned financial planners use both: they plan, they track, and they adjust. The key is consistency. If you keep at it, budgeting and expense tracking can become second nature—a cornerstone of financial wellness.

(This article is for educational purposes only and should not be considered financial advice. Always consult a licensed financial advisor for advice tailored to your specific circumstances.)

FAQs

Q1: Can I track expenses without a budget?

Yes, you can, but tracking alone won’t provide insight into whether your spending aligns with your financial goals.

Q2: How often should I update my budget?

Monthly is standard, but adjust whenever your income, expenses, or goals change significantly.

Q3: Are digital apps better than manual tracking?

Apps are convenient and automated, but manual tracking can increase awareness and mindfulness.

About Author

Jordan Maxwell is a personal finance educator with over a decade of experience helping beginners build strong financial habits. He specializes in practical budgeting techniques and tools for realistic money management.

References

[1] Mint. (2023). Expense tracking tips and tools.

[2] You Need A Budget. (2023). Budgeting 101: The basics of personal finance.

[3] Investopedia. (2023). Budgeting vs. expense tracking

Keep exploring our blog to uncover more practical tips for mastering your money and building financial confidence!

Recommend:

Protecting Your Investments from Inflation with TIPS and Floating-Rate Bonds

Budgeting for College Students: How to Stretch Every Dollar

Budget vs Expense Tracking: Understanding the Difference and Why You Need Both

Smart Moves: Exercising Employer Stock Options During Market Downturns Without Paying Excess Taxes