May 16, 2026

Key Takeaways:

● College students can manage finances effectively with a realistic budget.

● Tracking income and expenses is the first step toward financial control.

● Distinguishing between needs and wants prevents overspending.

● Using tools like spreadsheets or budgeting apps simplifies financial planning.

Estimated Reading Time: 18 minutes┃Post by: Jordan Fields

College is a time of growth, exploration, and independence—but also a period of financial risk. Between tuition fees, housing costs, textbooks, and social events, students can quickly find themselves living paycheck to paycheck. Without a strategy, even a modest income can vanish before the month ends.

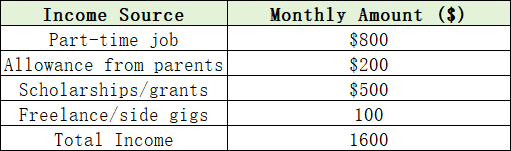

Step 1: Know Your Income Sources

A successful budget begins with a clear understanding of income. College students often have multiple streams, which can include:

Knowing your total monthly income ensures that your spending does not exceed available funds. For example, if your combined income is $1,600, your planned expenses should never surpass this amount, unless you have additional savings.

Tip: For irregular income, such as freelance earnings, calculate an average monthly figure based on the last three months. This prevents overspending during leaner months.

Step 2: Track Every Expense

Awareness of spending habits is essential. Divide expenses into fixed and variable categories:

Keeping a daily log of purchases—even $3 coffee runs—helps identify patterns and areas to cut back.

Step 3: Needs vs. Wants – Make Smart Decisions

Managing money in college starts with distinguishing needs from wants. Needs are essentials like rent, groceries, transportation, and textbooks—expenses that must be covered first. Wants are discretionary, such as dining out, subscriptions, or gadgets.

Before spending on a want, ask yourself: “Will this affect my ability to pay for essentials?” For example, buying a $60 video game when you only have $50 left for groceries is unwise.

You can also allocate specific amounts for discretionary spending. This lets you enjoy non-essential items while keeping your budget balanced and avoiding financial stress.

Step 4: Use Budgeting Tools

Tracking expenses manually can be tedious, but modern tools simplify this process:

1. Spreadsheets: Google Sheets or Excel can categorize income and expenses. Use formulas to automatically calculate totals and track remaining funds.

2. Apps: Mint, YNAB (You Need a Budget), or PocketGuard can connect to bank accounts and track spending automatically.

3. Envelope System: Allocate physical cash into envelopes for categories like groceries or entertainment. Spending is limited to what’s in each envelope.

Practical Tip: If you budget $100 for groceries and only spend $80, move the extra $20 into your savings envelope.

Step 5: Plan for the Unexpected

College life is unpredictable. Emergencies such as medical bills, urgent travel, or unexpected fees can arise. Even a small monthly contribution to an emergency fund—$50 per month—adds up over a semester to $300. This fund can cover minor emergencies without resorting to high-interest credit cards or loans. Example: Jordan’s laptop stopped working mid-semester. Having $300 saved allowed her to purchase a refurbished replacement without borrowing money or falling behind on assignments.

Step 6: Semester-Long Budget Planning

Instead of budgeting monthly, consider planning for an entire semester. This helps account for irregular but predictable expenses like textbooks or holiday travel.

This method helps avoid end-of-semester surprises when expenses spike due to gifts, travel, or extra supplies.

Step 7: Strategies to Reduce Expenses

Groceries: Buy store-brand products, meal prep, and use student discounts at local stores.

Transportation: Walk or bike to campus whenever possible. Public transportation passes can be cheaper than gas and parking fees.

Textbooks: Rent or purchase used books online. Some classes allow digital editions for significantly lower costs.

Entertainment: Attend free campus events or use student discounts for movies, concerts, and gyms.

Subscription Services: Rotate streaming subscriptions monthly instead of paying for all at once.

Step 8: Increase Income Wisely

While cutting costs helps, increasing income can make your budget less restrictive. Consider part-time campus jobs, tutoring, freelance work, or selling unused items like textbooks and electronics. Even small side earnings can cover discretionary expenses or boost your savings. For example, earning $150 a month from online tutoring can fund social activities while keeping essentials covered.

Step 9: Avoid Common Pitfalls

Students often fall into predictable money traps. Credit cards can build credit if paid in full, but accumulating debt is risky. Impulse purchases can derail a budget, so waiting 24 hours before non-essential buys is smart. Finally, always round up expense estimates to avoid surprises and stay on track.

Step 10: Review and Adjust Monthly

A budget isn’t static—it should adapt to real spending. Review each month: did you overspend on groceries, or save on transportation? Adjust the next month’s allocations accordingly. Flexibility keeps your finances realistic, reduces stress, and ensures you can enjoy college life without financial strain.

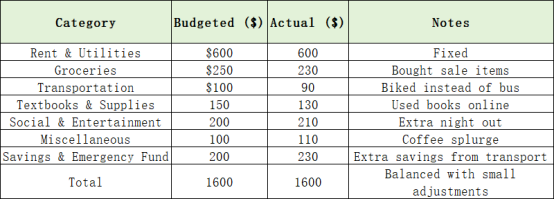

Realistic Example of a Student Budget

Even with minor overspending in social and miscellaneous categories, careful planning and small savings elsewhere maintain financial balance.

(This article is for informational purposes only and is not financial advice. Individual circumstances may vary; consult a financial advisor for personalized guidance.)

FAQs

Q1: Can I budget if I have irregular income?

Yes, prioritize essential expenses first and adjust discretionary spending monthly. Consider averaging your income over several months to smooth fluctuations.

Q2: How much should I save each month?

Even small amounts, like 10-15% of your monthly income, build a meaningful emergency fund over time.

Q3: Should I use credit cards as a student?

Only if you can pay the balance in full monthly. Credit cards can help build credit but can lead to debt if mismanaged.

About Author

Jordan Fields is a personal finance writer and former college student who successfully managed a tight budget while working part-time. With expertise in practical financial planning, student money management, and realistic expense tracking, Jordan empowers beginners to develop sustainable habits early.

References

[1] National Endowment for Financial Education. (2023). College student budgeting guide.

[2] Mint. (2023). How to budget for college students.

[3] U.S. News & World Report. (2022). Best ways to save money in college.

Stay on this blog to discover more practical strategies for making your money work as hard as you do while in college.

Recommend:

Budget vs Expense Tracking: Understanding the Difference and Why You Need Both

Snowball vs Avalanche Method: Which Debt Repayment Strategy Works Best for You?

How Robo-Advisors Can Build an ESG Micro-Portfolio Focused on Emerging Markets

Common Budgeting Mistakes and How to Avoid Them