May 8, 2026

In this Article:

● Inflation can erode the purchasing power of your investments if not proactively managed.

● Treasury Inflation-Protected Securities (TIPS) offer principal adjustments tied directly to inflation rates.

● Floating-rate notes (FRNs) provide protection against sudden interest rate spikes due to inflation.

● Combining TIPS and FRNs can create a balanced strategy for shielding a portfolio from inflation shocks.

Estimated Reading Time: 12 minutes┃Post by: Jordan Wells

The Inflation Risks and Portfolio Vulnerabilities

Inflation is often described as the silent wealth eroder. While a steady 2–3% inflation rate may seem manageable, sudden spikes—like the 7% surge observed in the U.S. in 2021—can significantly diminish the real value of cash and fixed-income investments. Imagine an investor with $100,000 in a traditional 10-year Treasury bond yielding 3%. If inflation unexpectedly jumps to 7%, the real return on that bond turns negative, effectively reducing the investor’s purchasing power.

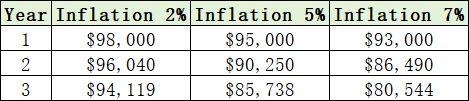

To illustrate this, consider a simplified table comparing the real value of $100,000 over three years under different inflation scenarios:

The table highlights how higher-than-expected inflation erodes capital faster than conventional bonds can compensate. For investors reliant on fixed-income instruments or retirees drawing down from a bond-heavy portfolio, sudden inflation surges can translate into real-world hardships—rising grocery bills, increased healthcare costs, and diminished retirement lifestyle.

Using TIPS to Counter Inflation

Treasury Inflation-Protected Securities, or TIPS, are U.S. government bonds explicitly designed to combat inflation. The principal of TIPS adjusts based on the Consumer Price Index (CPI), meaning that when inflation rises, the bond’s principal grows, ensuring the investor maintains purchasing power. Interest payments, which are a fixed percentage of the adjusted principal, automatically increase alongside inflation.

For example, suppose an investor purchases $50,000 of TIPS with a 1.5% coupon. If CPI inflation rises by 4% in a year, the principal adjusts to $52,000, and the annual interest becomes $780 instead of the original $750. While the nominal increase may appear small, over multiple years and in combination with larger allocations, TIPS can substantially reduce the real losses associated with inflation.

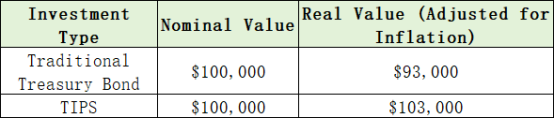

A realistic scenario can further illustrate TIPS in action. During the U.S. inflation surge of 2021:

Here, TIPS not only preserved purchasing power but also provided modest real gains. This example underscores the importance of including inflation-linked securities as part of a broader fixed-income allocation, especially for investors with a medium- to long-term horizon.

Incorporating Floating-Rate Notes for Additional Protection

Floating-rate notes (FRNs) are another effective tool to hedge against inflation. Unlike fixed-rate bonds, FRNs have coupon payments tied to short-term interest rates, such as the 13-week Treasury bill rate. When interest rates rise in response to inflationary pressures, FRN yields automatically adjust upward, reducing the risk of real losses.

Consider an investor holding $50,000 in a 2-year FRN with a spread of 0.25% above the benchmark rate. If short-term rates jump from 3% to 5%, the coupon adjusts from 3.25% to 5.25%, effectively preserving income relative to inflation. Unlike TIPS, which adjust principal, FRNs offer direct income adjustments and tend to react faster to central bank rate changes.

A combined approach—allocating 50% of a bond portfolio to TIPS and 50% to FRNs—can balance principal protection and income responsiveness. Historical back-testing demonstrates that such a strategy reduces volatility and maintains real returns more consistently during inflationary periods.

This hybrid approach showcases a realistic, actionable way for investors to hedge against inflation shocks while maintaining liquidity and exposure to rising interest rates.

Investors should also account for practical considerations, such as taxation of TIPS and FRN interest, liquidity in secondary markets, and appropriate maturity matching. Allocating based on risk tolerance, time horizon, and portfolio objectives is critical for achieving the desired inflation hedge without introducing excessive complexity or unintended risk.

Building a Practical Inflation-Defense Portfolio

For most individual investors, inflation protection works best when integrated gradually instead of implemented as an all-or-nothing bet.

Financial planners often suggest using inflation-sensitive assets as a stabilizing layer within the fixed-income allocation rather than replacing every traditional bond holding. The objective is not maximizing returns during inflationary periods; it is reducing the long-term erosion of purchasing power.

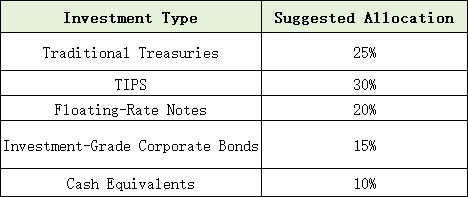

A sample moderate-risk allocation might look like this:

This structure attempts to balance three competing objectives:

1. Income stability

2. Inflation responsiveness

3. Capital preservation

Another important consideration is duration risk. Long-duration bonds suffer more when inflation expectations rise because future fixed payments become less attractive. Floating-rate notes reduce duration sensitivity since coupons reset regularly. Meanwhile, shorter-duration TIPS may experience less price volatility than long-term TIPS funds.

Tax treatment also deserves attention. TIPS principal adjustments are taxable annually even before maturity, creating what many investors call “phantom income.” Because of this, TIPS are often better suited for tax-advantaged accounts such as IRAs or retirement plans.

Investors should also understand that inflation protection is not solely about maximizing yield. During stable economic periods, TIPS frequently underperform conventional bonds because investors are paying for insurance against future inflation shocks. This tradeoff resembles homeowners insurance: most people hope they never need it, but the protection becomes invaluable during adverse conditions.

The following comparison illustrates long-term outcomes during different inflation cycles:

While nominal returns may appear similar, the inflation-adjusted results reveal the real benefit of inflation-sensitive investing.

There is also a psychological advantage. Investors with explicit inflation hedges often feel less pressure to react emotionally during inflationary headlines. Instead of chasing speculative trades or dramatically increasing stock exposure, they can rely on predetermined portfolio mechanisms designed specifically for inflation resilience.

Ultimately, the combination of TIPS and floating-rate notes works best as part of a disciplined, long-term investment framework. Inflation spikes are unpredictable, but portfolios can still be engineered to absorb them more effectively. Investors who prepare before inflation accelerates usually have more flexibility and less stress than those attempting to react after prices have already surged.

(This article is for informational purposes only and does not constitute financial advice. Investors should consult with a qualified financial advisor to tailor strategies to individual circumstances.)

FQAs

Q1: Are TIPS safe from inflation even if rates fall?

TIPS protect principal from inflation, but if deflation occurs, the principal adjusts downward. However, the U.S. Treasury guarantees that the final redemption value will not be less than the original principal.

Q2: Can FRNs underperform during periods of stable interest rates?

Yes, if short-term rates remain low, FRN yields may lag inflation. Combining FRNs with TIPS helps mitigate this risk.

Q3: How should I allocate between TIPS and FRNs?

Allocation depends on your risk tolerance, investment horizon, and income needs. A balanced starting point might be 50/50, adjusted based on personal circumstances.

About Author

Jordan Wells is a fixed-income strategist with over 15 years of experience in government securities and inflation-protected instruments. Jordan has advised both institutional and retail investors on portfolio construction strategies aimed at mitigating macroeconomic risks, particularly inflation and interest rate volatility.

References

[1] U.S. Department of the Treasury. (2026). Treasury Inflation-Protected Securities (TIPS).

[2] Investopedia. (2026). Floating-Rate Notes (FRNs).

[3] Federal Reserve Economic Data (FRED). (2026). Consumer Price Index for All Urban Consumers (CPI-U).

Explore more insightful strategies like this across our blog to safeguard your financial future in uncertain economic times.

Recommend:

The Self-Employed Guide to Safe, Smart Retirement Contributions

Smart Moves: Exercising Employer Stock Options During Market Downturns Without Paying Excess Taxes

How to Create a Budget for Beginners?

Frugal Living for Beginners: Practical Steps to Save Money and Live Well