May 6, 2026

In this Article:

● Frugal living doesn’t mean extreme deprivation; it’s about making mindful spending choices.

● Small daily changes can create big savings over time.

● Meal planning, budgeting, and smart shopping are foundational frugal strategies.

● Technology can simplify frugal living through apps and templates.

Estimated Reading Time: 15 minutes┃Post by: Emily Carter

Frugal living for beginners is about managing your money wisely while still enjoying life. It’s not about cutting out all fun or essentials but about making conscious decisions that save money without sacrificing quality. Frugality is more about mindful spending than deprivation. For example, choosing to brew coffee at home instead of buying a daily latte doesn’t reduce your happiness but can save hundreds of dollars a year. By adopting simple strategies, anyone can reduce unnecessary expenses, increase savings, and improve financial security.

Many beginners think frugal living requires complicated strategies or extreme austerity. In reality, the changes are small, manageable, and build over time. You don’t need to overhaul your lifestyle overnight; even minor adjustments—like reusing containers, switching off unused lights, or tracking spending—have cumulative financial impact.

Step-by-Step Tutorial

Step 1: Track Every Expense

Before saving, you need to know where your money goes. Start by listing all your monthly expenses in a spreadsheet, budgeting notebook, or app. Include fixed costs (rent, utilities, insurance) and variable costs (groceries, entertainment, coffee, subscriptions).

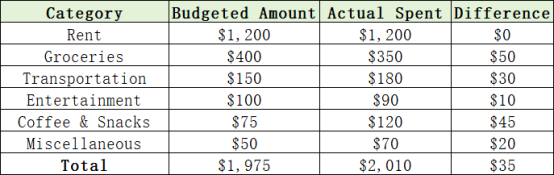

Example Table – Monthly Expenses

Tracking allows you to see where you consistently overspend and identify opportunities for adjustment. Most beginners are surprised by how small, regular purchases—like coffee, snacks, or ride-hailing services—add up to hundreds per month.

Step 2: Create a Realistic Budget

Once expenses are tracked, set a budget that allocates funds to essentials, savings, and discretionary spending. The 50/30/20 rule is a simple framework:

● 50% for needs (housing, groceries, transportation)

● 30% for wants (dining out, entertainment, hobbies)

● 20% for savings (emergency fund, retirement, debt repayment)

Tip: If 20% for savings feels high at first, start with 5–10% and gradually increase it over time. The key is consistency, not perfection.

Step 3: Meal Planning and Smart Grocery Shopping

Food expenses are often one of the easiest areas to save, but they require planning and commitment. Beginners may underestimate the impact of weekly habits like eating out or buying convenience foods.

Detailed Meal Planning Approach:

1. Create a Weekly Menu: Plan breakfast, lunch, dinner, and snacks. Include simple, repeatable meals to reduce decision fatigue.

2. Make a Grocery List: Stick strictly to the list to avoid impulse purchases. Divide items by store section to streamline shopping.

3. Buy in Bulk and Freeze: Purchase items like chicken, rice, or beans in bulk. Freeze portions for later to prevent spoilage and reduce cost-per-meal.

4. Use Seasonal Produce: Buying fruits and vegetables in season saves money and improves quality.

5. Minimize Waste: Save leftovers creatively. For example, leftover roasted vegetables can be turned into soups or sandwiches the next day.

Extra Tip: Track grocery spending in a notebook or app. Over 3–6 months, you’ll notice patterns and identify which meals are the most cost-effective.

Step 4: Reduce Recurring Costs

Recurring bills quietly drain money if not regularly reviewed. Frugal beginners often overlook this area because costs feel “fixed” or unavoidable.

Strategies to reduce recurring expenses:

Subscriptions: Make a list of all recurring services—streaming, cloud storage, gyms, magazines—and cancel unused or underused ones. Many people pay for subscriptions they haven’t used in months.

Utilities:

Switch to energy-efficient LED bulbs.

Reduce water consumption with low-flow showerheads.

Unplug appliances to prevent phantom electricity drain.

Adjust thermostat by 2–3 degrees; it can save 5–10% on heating or cooling.

Transportation:

Use public transport or carpool to save on gas.

Consider walking or cycling short distances; it reduces expenses and promotes health.

Evaluate if rideshare services can be minimized.

Insurance & Services: Review policies annually. Shop around for competitive rates on car, health, and home insurance—savings of $100–$300/year are possible.

Step 5: Adopt Mindful Lifestyle Habits (Expanded)

Frugal living goes beyond budgeting—it’s about creating habits that reduce unnecessary spending while enhancing life satisfaction.

DIY and Home Solutions:

Learn simple home repairs (e.g., fixing a leaky faucet or painting a wall) to avoid costly services.

Repurpose old furniture instead of buying new.

Frugal Entertainment:

Opt for free or low-cost leisure options: hiking, community events, libraries, local festivals.

Host potlucks or game nights instead of dining out; social enjoyment remains, costs drop.

Impulse Control:

Apply the 24-hour rule for non-essential purchases. Waiting reduces impulsive buying and buyer’s remorse.

Use cash envelopes for discretionary spending; physically seeing money limits overspending.

Community Sharing:

Swap clothing, books, or tools with friends or neighbors. Join free local skill-sharing workshops.

Step 6: Leverage Seasonal and Long-Term Savings (Expanded)

Frugality is strategic. Timing purchases, planning for the year, and investing in long-term solutions amplify savings.

Seasonal Shopping: Buy clothes, gifts, or household items during clearance periods. Off-season purchases often cut costs by 20–50%.

Annual Sales Planning: Plan major purchases around Black Friday, back-to-school sales, or holiday promotions to maximize discounts.

Invest in Energy Efficiency:

Programmable thermostats, low-flow faucets, and insulation reduce utility bills over time.

Even small upfront costs can save hundreds annually.

Bulk & Subscription Savings:

Join bulk-buying programs for cleaning products or pantry staples.

Consider subscription services for essential consumables (e.g., razors, vitamins) that offer discounts.

Illustrative Example: Buying 6 months’ worth of household staples during seasonal sales: $200 saved annually.

Advanced Tips for Sustainable Frugal Living

Beyond basic tracking and budgeting, frugal living benefits from small, everyday practices that make savings automatic and lifestyle-friendly. Simple energy-saving measures, like running appliances during off-peak hours or lowering heating slightly in winter, reduce monthly bills. Meal prepping, batch cooking, and repurposing leftovers help reduce both grocery costs and food waste.

Community-based frugal habits, such as swapping clothes, books, or toys with neighbors, attending free workshops, and using public resources like libraries, provide entertainment and value at minimal cost. Smart transportation choices, including walking, biking, or using multi-pass transit cards, also reduce expenses while benefiting health and the environment. Regularly reviewing phone plans, internet packages, and other subscriptions ensures you only pay for services you actually use.

Ultimately, frugality is less about restriction and more about aligning spending with your values. By focusing on priorities, planning purchases, and making conscious decisions, beginners can enjoy a high-quality lifestyle while improving financial security. Over time, these habits accumulate, creating a foundation for emergency savings, investments, and long-term financial freedom.

(The information in this article is for educational purposes and does not constitute financial advice. Always consult a certified financial advisor for personalized guidance.)

FAQs

Q1: Can frugal living be sustainable long-term without feeling restricted?

Yes. By prioritizing essential spending and finding cost-effective alternatives for discretionary items, frugality becomes a lifestyle rather than deprivation.

Q2: How quickly can I expect savings from frugal changes?

Most people notice savings within one to two months of consistent tracking and habit adjustments.

Q3: Can frugal living coexist with investing and building wealth?

Absolutely. Frugality frees up money that can be redirected toward investments, retirement funds, and emergency savings.

About Author

Emily Carter is a certified personal finance coach with over 8 years of experience helping beginners create actionable budgets, save consistently, and adopt sustainable financial habits. She specializes in practical frugal strategies tailored for real-life scenarios, including meal planning, smart shopping, and lifestyle optimization for financial wellness.

References

[1] DaveRamsey.com. (2023). Frugal Living Tips.

[2] NerdWallet. (2023). Budgeting for Beginners: A Complete Guide.

[3] Investopedia. (2023). Frugal Living: How to Save Money Without Sacrificing Life.

Explore more beginner-friendly personal finance guides to take control of your money today!

Recommend:

Budget vs Expense Tracking: Understanding the Difference and Why You Need Both

The Retirement Healthcare Strategy Most Americans Overlook: Maximizing Your HSA

Why Your Paycheck Disappears Before Rent?

Snowball vs Avalanche Method: Which Debt Repayment Strategy Works Best for You?