May 9, 2026

Key Highlights:

● Saving money on a low income is possible with small, consistent changes to daily habits.

● Budgeting is the foundation for finding and directing even a small amount of money toward savings.

● Prioritizing needs over wants and finding cost-effective alternatives helps stretch every dollar.

● Emotional and lifestyle adjustments play a crucial role in building financial stability on a tight budget.

Estimated Reading Time: 12 minutes┃Post by: Emma Caldwell

Living on a low income can make saving money feel impossible. Rent, groceries, bills, and transportation costs can quickly consume every paycheck, leaving little room for financial growth. Yet, many people in similar situations have successfully built savings and even started investing, all while earning modest wages. The key lies in understanding where money is going, making deliberate choices, and finding creative ways to stretch every dollar. This article provides realistic, actionable strategies for saving money on a low income, complete with tables, figures, and examples grounded in real-world scenarios.

1. Assessing Your Current Financial Situation

Before any money-saving plan can succeed, you need to understand your current financial reality. Start by tracking every expense for at least one month, including recurring bills, groceries, transportation, and discretionary spending.

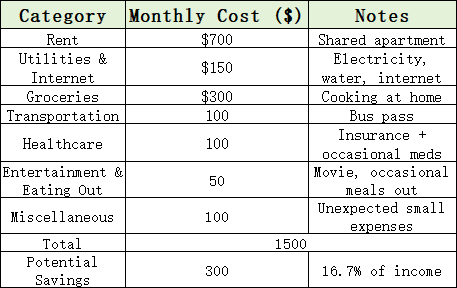

Even on a low income, you can identify potential savings of nearly 17% of your paycheck with careful review.

2. Creating a Realistic Budget

Budgeting on a low income requires a practical approach. Traditional budgeting rules like the 50/30/20 split may not be feasible if fixed costs take up the majority of your income. Instead, try a priority-based budget:

● Essential needs first: Rent, utilities, groceries, transportation.

● Debt repayments next: Avoid late fees that can snowball.

● Savings last: Even $20 a month builds over time.

Example Table: Priority-Based Low-Income Budget

Consistency matters more than perfection. Even small contributions to savings can prevent financial emergencies from derailing your budget.

3. Reducing Everyday Expenses

Small changes in daily habits can lead to meaningful savings. Here are realistic strategies:

● Groceries: Buy store brands, use coupons, plan meals to avoid waste.

● Utilities: Unplug electronics when not in use, adjust thermostat, and monitor water usage.

● Transportation: Consider public transport, carpooling, or biking when feasible.

● Entertainment: Free local events, library resources, and streaming services can replace costly outings.

4. Leveraging Community Resources

Even those on a low income can access community resources that reduce everyday expenses. Food banks, community centers, and local non-profits often provide free or discounted goods. Some employers offer transportation subsidies or financial wellness perks. Online cashback applications, rewards programs, and coupon websites can provide additional incremental savings. A household spending $300 per month on groceries could save approximately $6 each month through a combination of cashback apps and loyalty coupons. While the amount may seem small, it accumulates over time and contributes to a growing financial buffer.Even on a low income, you can tap into resources that reduce expenses:

● Food banks, community centers, and local non-profits often provide free or discounted goods.

● Employer programs may offer transportation subsidies or financial wellness perks.

● Online cashback apps, rewards programs, and coupon websites provide incremental savings.

Example: Using a combination of a cashback app (2% return on grocery spending) and loyalty coupons, a household spending $300 per month on groceries could save $6 monthly. Small amounts compound over time.

5. Building an Emergency Fund

Low-income earners are particularly vulnerable to unexpected expenses. Even a $500 emergency fund can prevent a minor car repair or medical bill from turning into debt. Start small:

● Save $10–$20 per paycheck until your fund reaches $500.

● Keep funds in an easily accessible, separate savings account to avoid spending temptation.

6. Finding Extra Income Opportunities

While saving is critical, supplementing income can accelerate financial stability. Side income opportunities, such as freelancing, tutoring, or part-time weekend work, can provide extra cash. Selling unused items online or participating in survey panels and cashback programs for everyday spending are also viable options. Freelancing, tutoring, or part-time weekend work.

● Selling unused items online.

● Participating in survey panels or cashback programs for everyday spending.

Example Scenario: A person earning $1,800 monthly can supplement their income by $100 per month through part-time work or side hustles, effectively boosting potential monthly savings to $400.

7. Adjusting Mindset and Lifestyle

Money management is as much psychological as it is numerical. Low-income earners must cultivate habits of patience, discipline, and long-term thinking:

● Focus on small wins: celebrating $50 saved may encourage more consistent savings.

● Avoid comparison with higher-income peers; set realistic goals for your situation.

● Recognize that every dollar saved contributes to future financial stability.

Illustrative Tip: Tracking progress visually, such as filling a savings jar or spreadsheet, can make growth tangible and motivate ongoing commitment.

Saving money on a low income is challenging but achievable with practical strategies, realistic budgeting, and consistent effort. By combining careful expense tracking, prioritization, community resources, and small lifestyle adjustments, anyone can build a financial safety net. Remember, progress is more important than perfection—each small step contributes to long-term stability.

(The content in this article is for educational purposes only and should not be considered personalized financial advice. Everyone’s financial situation is different, and decisions regarding budgeting, saving, or debt carry risks. The strategies shared here are general tips that have helped many low-income earners, but results may vary. Readers should research, consider their circumstances, and consult a certified financial advisor before making financial decisions. The author and this website are not responsible for any outcomes resulting from applying this information.)

FAQs

Q1: How much should I aim to save each month on a low income?

Even saving 5–10% of your monthly income is meaningful. The key is consistency and gradually increasing savings as possible.

Q2: Can I save money without cutting back on everything I enjoy?

Yes. Focus on cost-effective alternatives for discretionary spending, such as free entertainment or meal planning, rather than eliminating enjoyment entirely.

Q3: How do I handle debt while trying to save on a low income?

Prioritize minimum payments to avoid penalties while allocating a small portion of income to savings. Over time, you can increase debt repayments as savings grow.

About Author

Emma Caldwell is a personal finance educator with over ten years of experience helping individuals and families improve their financial literacy. She specializes in practical budgeting, saving strategies, and building financial resilience for low- and middle-income households. Emma combines realistic advice with an understanding of the emotional challenges of managing money on a tight budget. She contributes regularly to financial literacy blogs and workshops, aiming to make personal finance accessible and achievable for everyone.

References

[1] Financial Literacy and Education Commission. (2023). Budgeting basics for low-income households.

[2] Consumer Financial Protection Bureau. (2022). Managing expenses on a tight budget.

Explore more practical personal finance tips on this blog to keep building financial stability, no matter your income.

Recommend:

How Robo-Advisors Can Build an ESG Micro-Portfolio Focused on Emerging Markets

How Low-Interest Personal Loans Can Simplify Your Finances Without Harming Your Credit

The Realistic Timeline to Becoming Debt-Free: Step-by-Step Guide for Beginners

How Freelancers Can Avoid Hidden FX Fees When Getting Paid Internationally