May 12, 2026

Key Takeaways:

● The time to become debt-free depends on total debt, interest rates, and repayment strategy.

● Making consistent, above-minimum payments accelerates the journey to financial freedom.

● Snowball and avalanche methods are two effective approaches for debt repayment.

● Tracking progress with budgeting apps and templates improves discipline and motivation.

● Realistic planning and small sacrifices can help you achieve debt freedom faster.

Estimated Reading Time: 16 minutes┃Post by: Emma Carson

The time it takes to be debt-free varies widely depending on your total debt, monthly payment capacity, interest rates, and repayment strategy. For example, someone with $10,000 in credit card debt paying only the minimum could take 10–15 years to pay it off, whereas a focused plan with extra payments could reduce that to 2–3 years. Achieving debt freedom is less about a fixed timeline and more about creating a realistic, actionable plan that fits your financial situation.

Debt freedom is not simply a mathematical exercise—it’s a lifestyle adjustment. The journey often involves tough but manageable decisions, such as temporarily reducing discretionary spending, prioritizing high-interest debts, and creating a realistic emergency fund to prevent future borrowing. The sooner you start, the shorter your journey will be, and the more interest you will save over time.

Step-by-Step Tutorial: How to Calculate Your Path to Debt Freedom

Step 1: List all debts

Create a table of all outstanding debts, including creditor, balance, interest rate, and minimum monthly payment. This allows you to see your debt landscape clearly.

Listing debts this way highlights where your money is going and which debts cost you the most in interest. Without this clarity, repayment strategies can be haphazard and slow.

Step 2: Determine your monthly payment capacity

Review your monthly income and expenses. Identify discretionary spending that can be redirected to debt repayment. For example, dining out, subscription services, and nonessential shopping could free up $300–$500 per month.

If your current budget is tight, start small but commit to incremental increases as possible. For example:

● Extra $50 per month → small reduction in timeline

● Extra $200 per month → noticeable acceleration

● Extra $500+ per month → significant reduction in debt timeline

Your repayment capacity is your monthly “weapon” against debt. The more consistent and aggressive, the faster your freedom.

Step 3: Choose a repayment strategy

Two popular strategies dominate:

● Avalanche method: Pay off the debt with the highest interest rate first while making minimum payments on others. This approach reduces total interest paid over time.

● Snowball method: Pay off the smallest balance first to gain psychological momentum, motivating you to tackle bigger debts.

Both methods work, and the right choice depends on whether you are motivated by interest savings or early wins. For many beginners, a hybrid approach works best—start with a small win, then switch to avalanche for efficiency.

Step 4: Calculate repayment timeline

You can use online debt calculators, spreadsheets, or apps to calculate payoff timelines. For a realistic scenario, consider:

● Debt Total: $15,500

● Monthly Payment Capacity: $1,000

● Weighted Interest Rate: 14%

By paying $1,000 per month using the avalanche method, you could be debt-free in about 24 months. Paying only minimums, however, could extend the timeline to 5–6 years and cost over $6,000 in interest.

Step 5: Adjust and monitor

Repayment is a living plan, not a one-time calculation. Review your budget monthly. Life events like bonus payments, tax refunds, or reduced expenses should go straight to debt. Likewise, unexpected expenses may temporarily slow your progress—plan for this by keeping a small emergency fund.

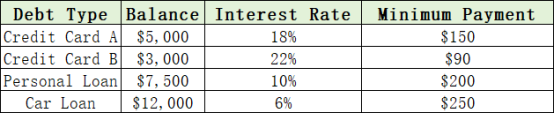

Hypothetical Case Study

Meet Sarah:

● Total Debt: $15,500

● Monthly Income: $3,500

● Monthly Expenses: $2,500

● Repayment Capacity: $1,000

Sarah uses the avalanche method:

● Highest interest: Credit Card B at 22%

● Next: Credit Card A at 18%

● Lowest: Personal Loan at 10%

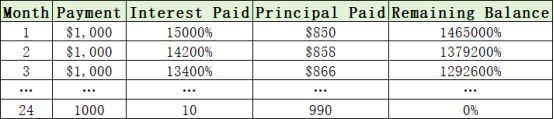

Projected Timeline:

By month 24, Sarah is debt-free. Without extra payments, her timeline could have been 5–6 years. This case highlights how even moderate extra payments accelerate payoff dramatically and reduce interest costs.

Life events can alter the timeline. If Sarah faces a $500 car repair, she may temporarily reduce payments, extending her payoff by 1–2 months. Planning for such contingencies ensures the plan remains achievable without stress.

Tools: Apps/Templates

Using tools improves accountability and visualization of progress. Here are practical tools for beginners:

● Debt Payoff Planner (App): Tracks multiple debts, calculates payoff schedules, and shows interest saved using different strategies.

● YNAB (You Need a Budget): Allocates extra cash toward debt and tracks every dollar, helping avoid overspending.

● Mint: Free tool to track debts, categorize spending, and receive alerts for upcoming payments.

● Excel Templates: Create a custom debt tracker, visualize monthly balances, principal vs. interest, and projected payoff dates.

Sample Debt Tracker Template:

Using such tools provides tangible progress, making the journey more motivating and realistic.

Tips to Speed Up Debt Repayment

1. Reduce high-interest spending: Avoid new credit card charges.

2. Automate payments: Ensures you never miss a payment and prevents late fees.

3. Increase income streams: Side hustles or freelancing can provide extra repayment funds.

4. Cut unnecessary expenses: Small sacrifices (coffee, subscriptions, dining out) can be redirected to debt.

5. Stay disciplined: The hardest part is sustaining consistency, not calculating numbers.

(The information provided in this article is for educational purposes only and does not constitute professional financial advice. While the strategies and examples are based on widely accepted personal finance principles, individual results may vary depending on factors such as income, expenses, debt types, and interest rates. Readers should carefully assess their own financial situation before implementing any suggestions and consider consulting a certified financial advisor for personalized guidance. The author is not responsible for any financial losses, missed payments, or other outcomes resulting from the use of this content, tools, or resources mentioned.)

FAQs

Q1: Can I become debt-free faster than planned?

Yes. Extra income, reduced expenses, or one-time payments (like tax refunds or bonuses) can shorten the timeline significantly.

Q2: Which repayment method saves more money?

The avalanche method generally saves more on interest, while the snowball method offers psychological motivation that can help prevent early abandonment of the plan.

Q3: What if my debt includes variable interest rates?

Regularly update your repayment plan to reflect rate changes, ensuring you target the most costly debt first and avoid surprises.

About Author

Emma Carson is a personal finance coach with over 8 years of experience helping beginners achieve debt freedom. She specializes in budgeting, debt repayment strategies, and practical financial planning for everyday people. Emma’s mission is to turn overwhelming debt situations into manageable, realistic plans that lead to long-term financial stability.

References

[1] Federal Reserve. (2023). Consumer Credit – G.19.

[2] NerdWallet. (2024). Debt Payoff Strategies.

[3] Investopedia. (2024). Snowball vs. Avalanche Method.

Explore more articles on this blog to learn strategies for saving, investing, and achieving complete financial freedom.

Recommend:

How Student Loan Forgiveness Can Become a Down Payment for Real Estate Investing

Smart Moves: Exercising Employer Stock Options During Market Downturns Without Paying Excess Taxes

The Self-Employed Guide to Safe, Smart Retirement Contributions

How to Create a Budget for Beginners?