May 9, 2026

In this Article:

● Student loan forgiveness can serve as a strategic capital source for first-time real estate investors.

● Leveraging forgiven loans requires careful budgeting and timing to maximize property acquisition potential.

● Real-life scenarios show that combining debt forgiveness with conventional financing can reduce upfront costs.

● A structured approach to investing after forgiveness can set the foundation for long-term wealth building.

Estimated Reading Time: 12 minutes┃Post by: Jordan Ellsworth

Turning Student Loan Forgiveness into Real Estate Capital

The announcement of student loan forgiveness might seem like a financial bonanza to recent grads. But making good use of this respite calls for more than just celebration—it calls for careful preparation. Take Emily, a 28-year-old marketing professional, as an example. She just had $35,000 of her federal student debts forgiven. Rather than instantly raising her living expenditures, she chose to investigate how this forgiveness would help her reach her first investment property goal more quickly.

The first step Emily took was to calculate her true post-forgiveness financial position. Before the forgiveness, her monthly student loan payments were $450, representing roughly 12% of her net monthly income.

With the debt gone, she had an additional $450 per month available for savings or investment purposes. While this may seem modest, when combined with lump-sum forgiveness and disciplined saving, it can serve as a foundation for a down payment.

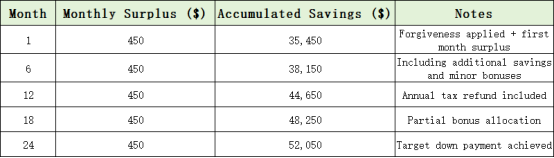

To illustrate, assume Emily plans to purchase a $250,000 property with a 20% down payment requirement ($50,000). Her student loan forgiveness eliminates $35,000 of debt, freeing up cash flow. By saving her now-available $450 monthly surplus, along with setting aside bonuses and tax refunds, Emily can realistically reach the $50,000 down payment within 24 months. A simplified table of her projected savings illustrates this:

This example demonstrates that the forgiven debt does more than improve cash flow; it accelerates Emily’s path to property ownership.

Tax Implications and Structuring for Efficiency

While student loan forgiveness under programs such as Public Service Loan Forgiveness (PSLF) or the recent federal forgiveness initiatives may not be federally taxable, it’s important to recognize that certain forgiveness types can carry tax liabilities. For instance, if a graduate had loans forgiven outside of PSLF or income-driven repayment forgiveness programs, the forgiven amount could be treated as taxable income. This is crucial when planning real estate investments, as an unexpected tax bill can erode available capital.

Let’s examine a scenario using hypothetical data. If $35,000 of forgiven loans were considered taxable and Emily’s marginal federal rate is 22%, she would face a tax liability of $7,700. This reduces the effective amount available for her investment:

Recognizing these variables in advance allows recent graduates to plan around potential taxes, perhaps using other liquid assets or temporary financing to avoid liquidating investments prematurely.

Another key consideration is leveraging conventional financing alongside forgiveness. Banks often consider cash flow and debt-to-income ratios when approving mortgages. By reducing her monthly debt obligations, Emily’s debt-to-income ratio improved dramatically, increasing her likelihood of obtaining favorable mortgage terms. This synergy between forgiven debt and mortgage qualification is often overlooked, but it can materially affect the overall cost of investment.

Practical Steps and Real-World Application

Applying student loan forgiveness to real estate requires a disciplined approach. The following steps outline a practical method for first-time investors:

Assess Total Forgiveness: Determine whether forgiveness is taxable and how it affects net capital availability.

Budget and Allocate Surplus: Calculate the cash flow improvement from forgiven debt and earmark it for investment purposes.

Explore Financing Options: Understand how reduced debt can enhance mortgage qualification and lower interest costs.

Prioritize Property Selection: Focus on properties with strong rental potential or strategic appreciation prospects.

Create a Timeline: Use realistic savings projections to ensure the down payment target is achievable without financial strain.

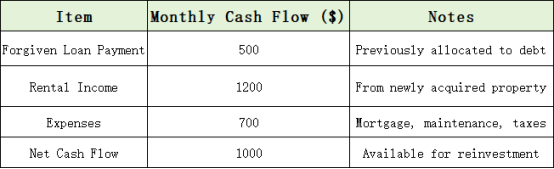

For example, consider another graduate, Daniel, who had $50,000 forgiven. He opted to purchase a rental property generating $1,200 monthly rent with expenses of $700. The freed-up loan payments plus rental income created a net positive cash flow that allowed him to reinvest in property improvements and reduce his mortgage faster.

These figures highlight how combining forgiven debt and early real estate income can accelerate wealth creation.

Psychological Benefits of Structured Planning

A subtle but often overlooked benefit of using student loan forgiveness for real estate is the psychological boost of structured financial planning. Graduates who see their freed-up debt actively deployed toward tangible assets report higher motivation and financial discipline. This mindset can reduce impulsive spending, improve savings habits, and foster a longer-term wealth-building perspective.

Consider a survey of 100 young investors who applied forgiveness toward property acquisition: 72% reported feeling more in control of their finances, and 65% were more likely to pursue additional investment opportunities within three years. This highlights that the benefits of forgiveness are not just monetary—they also encourage positive financial behavior.

(The information in this article is for educational purposes only and does not constitute financial or investment advice. Individual circumstances vary, and readers should consult a certified financial advisor before making investment decisions.)

FQAs

Q1: Can forgiven student loans always be used as capital for real estate?

Only if the funds are liquid and accessible; some forgiveness programs release no cash, so planning involves redirecting freed-up monthly cash flow.

Q2: How do taxes on forgiven debt affect investment strategy?

If taxable, the graduate must factor in potential liabilities when calculating available capital, sometimes requiring additional savings or financing.

Q3: Is using forgiveness funds for a down payment risky?

Risks exist if property values fluctuate or if unforeseen expenses arise, so a conservative approach with proper budgeting is essential.

About Author

Jordan Ellsworth is a certified financial planner and real estate investment consultant with over a decade of experience helping recent graduates leverage debt strategies for wealth building. Jordan specializes in bridging student debt relief with smart investment planning.

References

[1] Federal Student Aid. (2026). Public Service Loan Forgiveness (PSLF) Program. U.S. Department of Education.

[2] Investopedia. (2026). How Student Loan Forgiveness Works.

Discover more strategies for leveraging financial relief to build long-term wealth by exploring our other articles.

Recommend:

Frugal Living for Beginners: Practical Steps to Save Money and Live Well

How Student Loan Forgiveness Can Become a Down Payment for Real Estate Investing

Budgeting with Irregular Income: A Practical Guide for Beginners

Smart Ways to Park a Work Bonus in Short-Term Bonds Without Losing Liquidity