May 17, 2026

Key Highlights:

● Budgeting with irregular income requires tracking income and expenses closely.

● Establishing a baseline monthly budget based on the lowest expected income ensures stability.

● Prioritizing essential expenses and creating a buffer or “rainy day” fund prevents financial stress.

● Flexible budgeting strategies allow for saving, debt repayment, and occasional discretionary spending.

● Using real-world tools and scenarios makes managing fluctuating income practical and sustainable.

Estimated Reading Time: 18 minutes┃Post by: Riley Thompson

For anyone earning a paycheck that varies month to month—freelancers, gig workers, commission-based employees, or seasonal workers—budgeting can feel like walking a financial tightrope. Unlike fixed-salary earners, irregular income introduces uncertainty that can quickly lead to missed bills, overspending, or stunted savings. However, with a structured approach, managing fluctuating income is entirely possible, and even empowering.

Step 1: Track Your Income and Expenses Meticulously

The foundation of budgeting with irregular income is precise tracking. Start by reviewing your income over the past 12 months. Document the highest, lowest, and average monthly earnings. This step will allow you to set realistic expectations and avoid budgeting based on optimism.

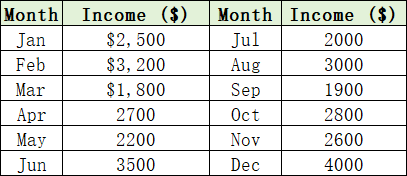

Example Table: Monthly Income Overview

From this table, it’s clear that the lowest month is $1,800, while the highest reaches $4,000. Using your lowest income as a baseline ensures your essential expenses are always covered.

Next, categorize your expenses into three groups:

1. Essential: Rent/mortgage, utilities, groceries, transportation, insurance.

2. Variable: Gas, dining out, entertainment, clothing.

3. Optional/Discretionary: Subscriptions, vacations, luxury items.

Tracking these expenses over several months will reveal patterns, helping you anticipate and manage future fluctuations.

Step 2: Set a Baseline Budget

Using your lowest monthly income as a benchmark, create a budget that covers only essential expenses. This baseline ensures that even in lean months, bills are paid, and stress is minimized.

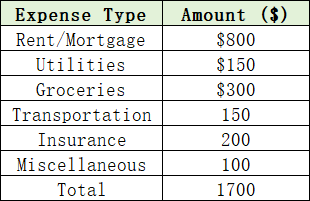

Example Baseline Monthly Budget (for $1,800 month):

This leaves a small buffer ($100) for unexpected costs. This conservative baseline approach prevents overspending and creates a foundation for managing variable months effectively.

Step 3: Build an Emergency Buffer

Irregular income demands a financial cushion. Ideally, aim to save at least 3–6 months of essential expenses.

Example Calculation:

● Baseline monthly expenses: $1,700

● Emergency fund goal: 3–6 months

● Total: $5,100 – $10,200

In practical terms, if you earn $3,500 in a strong month, allocate a portion of that surplus to your emergency fund before spending on anything else. This strategy ensures lean months are manageable without relying on credit cards or loans.

Step 4: Prioritize Income Allocation in High-Earning Months

During high-income months, treat extra money strategically rather than as a free-for-all. Allocate surplus funds in priority order:

Emergency Fund: Top priority until your buffer is fully funded.

Debt Repayment: Use extra income to pay off high-interest debt quickly.

Savings and Investments: Fund retirement accounts or other long-term goals.

Discretionary Spending: Only after essentials, savings, and debt obligations are covered.

Scenario Example: Monthly income: $3,500/Baseline expenses: $1,700/Surplus: $1,800

Allocation plan: 50% to savings/emergency fund ($900)/30% to debt repayment ($540)/20% to discretionary spending ($360)

This method balances financial security with lifestyle flexibility.

Step 5: Use Practical Tools to Smooth Income Variability

1. Multiple Accounts Strategy

Maintain separate accounts for essentials, taxes, and discretionary spending. By compartmentalizing your money, it’s easier to avoid accidental overspending and ensure bills are always covered.

2. Rolling Budget

Carry over surplus funds from high-income months to low-income months. This approach provides predictability and reduces stress when income dips.

3. Zero-Based Budgeting

Assign every dollar a specific purpose each month. This technique ensures all income is accounted for, minimizing waste and maximizing control.

4. Automated Transfers

Set up automatic transfers to savings and bill accounts as soon as income arrives. Automation reduces the temptation to spend surpluses impulsively.

Real-World Scenarios

Case Study 1 – Freelancer Jamie:

Jamie, a freelance graphic designer, earns anywhere from $2,000 to $5,000 monthly. By setting a baseline budget at $2,200, Jamie uses surplus income to fund an “overflow account” for lean months and quarterly taxes. The result: financial stability and predictable discretionary spending.

Case Study 2 – Seasonal Worker Maria:

Maria works at a summer resort earning $4,000 per month for four months and $1,000 per month during off-season. She divides her summer earnings:

● 50% for off-season expenses ($2,000/month for four months)

● 20% into savings ($800/month)

● 30% for discretionary spending and extra payments ($1,200/month)

By planning ahead, Maria covers year-round living costs without stress.

Step 6: Manage Mindset and Lifestyle Expectations

Budgeting with irregular income isn’t just about numbers—it requires discipline and realistic expectations. It’s common for irregular earners to experience emotional highs and lows linked to income swings. Establishing routines for saving, spending, and monitoring your finances reduces anxiety and builds confidence over time.

Tip: Focus on stability rather than matching lifestyle to peak income months. Avoid lifestyle inflation in high-earning months; this ensures your financial plan remains sustainable.

Step 7: Regularly Review and Adjust

Budgeting with irregular income requires ongoing attention. At the end of each month, compare your actual income with projections to see if your baseline budget is realistic. Track patterns in your earnings to anticipate lean months and allocate surplus income effectively. Adjust your savings, spending, and discretionary funds as needed, increasing contributions in high-income months and cutting back during slower periods. Treat your budget as a flexible tool, reviewing it monthly to maintain control and reduce financial stress.

(This article is for informational purposes only and does not constitute personalized financial advice. Readers should consult a licensed financial advisor for tailored guidance.)

FAQs

Q1: How do I handle months with zero income?

Use your emergency fund to cover essential expenses and adjust discretionary spending accordingly. Plan ahead by saving extra in high-income months.

Q2: Should I pay taxes monthly or quarterly with irregular income?

Self-employed and freelance individuals should consider quarterly estimated tax payments to prevent large end-of-year obligations.

Q3: Can irregular income support long-term financial goals like buying a house?

Yes, but it requires disciplined saving, a robust emergency fund, and conservative planning based on average or low-income months rather than peak months.

About Author

Riley Thompson is a financial educator and freelance consultant with over a decade of experience helping individuals and small business owners manage unpredictable incomes. Riley emphasizes realistic budgeting, sustainable savings strategies, and practical financial tools tailored to irregular earners.

References

[1] Dave Ramsey. (2023). Budgeting for irregular income.

[2] IRS. (2023). Estimated Taxes for Self-Employed Individuals.

[3] NerdWallet. (2023). How to Budget With Irregular Income.

Take control of your finances today—explore more articles on this blog to find practical strategies for managing money, building wealth, and thriving with any income type.

Recommend:

Smart Moves: Exercising Employer Stock Options During Market Downturns Without Paying Excess Taxes

Frugal Living for Beginners: Practical Steps to Save Money and Live Well

How Robo-Advisors Can Build an ESG Micro-Portfolio Focused on Emerging Markets

How Long It Really Takes to Build Your Credit?