May 11, 2026

Key Takeaways:

● Remote workers and digital nomads often face high fees when converting currencies for international payments.

● Multi-currency bank accounts can drastically reduce these conversion costs and save hundreds per year.

● Proper planning can make global freelancing more profitable and less financially stressful.

Estimated Reading Time: 12 minutes┃Post by: Alex Mercer

Why Currency Conversion Fees Matter for Remote Workers

For remote workers earning in multiple currencies, the hidden cost of currency conversion can quietly erode income. Consider Sarah, a freelance graphic designer based in Thailand who contracts with clients in the U.S., Germany, and Australia. Last year, she earned the equivalent of $50,000 USD, but due to frequent conversions from USD and EUR to Thai Baht, she lost over $1,200 in fees alone. This scenario is not unusual—data from TransferWise (now Wise, 2023) indicates that average bank conversion fees range from 2% to 3% per transaction.

Multi-currency bank accounts are designed to mitigate these costs. Unlike traditional accounts, they allow a freelancer to hold funds in multiple currencies without immediate conversion, providing flexibility to convert when exchange rates are favorable.

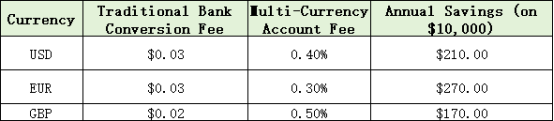

This table illustrates that even moderate annual earnings in multiple currencies can benefit significantly from multi-currency accounts.

How Multi-Currency Accounts Work in Real Life

Multi-currency accounts function as a single digital wallet with sub-accounts for each currency. Users can receive payments directly in the currency they are invoiced in and hold that balance until a favorable exchange rate is available. For instance, Javier, a remote marketing consultant based in Mexico, receives monthly payments in USD and GBP. By using a multi-currency account, he holds his USD balance until the peso strengthens, then converts it—saving hundreds over the year.

Some platforms even integrate with payment processors like PayPal, Stripe, or direct bank transfers, allowing remote workers to bypass traditional bank conversion entirely. Additionally, many accounts offer free or low-cost international transfers between peers, which can be particularly advantageous for freelancers paying overseas contractors or subscribing to foreign software services.

Consider the following scenario comparing traditional banking versus multi-currency banking:

Scenario:

● Remote worker receives $5,000 USD per month from an international client.

● Bank conversion rate includes 2.5% fee.

● Multi-currency account conversion fee: 0.4%

Traditional Bank: $5,000 - 2.5% = $4,875 converted to local currency

Multi-Currency Account: $5,000 - 0.4% = $4,980 converted to local currency

Over 12 months, the worker saves $1,260—a non-trivial sum for freelancers.

Multi-currency accounts are particularly practical for remote workers who:

● Frequently receive payments in more than one currency.

● Travel regularly and need access to local funds.

● Aim to optimize tax reporting across multiple countries by tracking payments in original currencies.

It is important to note, however, that multi-currency accounts are not entirely free of costs. Some banks may charge monthly maintenance fees, while others may have limits on free conversions. Understanding these nuances is critical to maximizing benefits.

Using Exchange Rates to Your Advantage

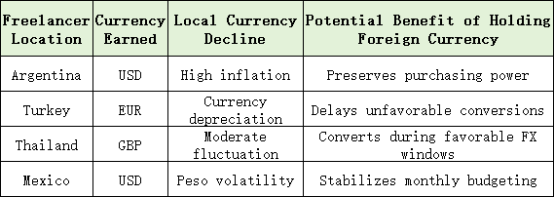

One overlooked advantage of multi-currency bank accounts is their ability to help remote workers manage exchange-rate volatility, not just transaction fees. Many freelancers focus only on the percentage charged during conversion, but the timing of currency exchanges can significantly impact annual earnings. A remote software developer earning in USD while living in Argentina, for example, may see monthly income fluctuate dramatically depending on exchange-rate movements. By holding funds in USD inside a multi-currency account and converting only when local currency conditions improve, workers gain more control over purchasing power. Industry comparisons show that traditional banks often embed hidden FX markups of 2–4%, while fintech multi-currency platforms may reduce those costs below 1%.

Another important dimension is invoice strategy. Experienced freelancers increasingly invoice clients in “stronger” currencies such as USD, EUR, or GBP while maintaining local spending accounts separately. This minimizes exposure to weaker domestic currencies and creates a natural hedge against inflation. In online remote-work communities, many digital nomads describe using accounts that provide local banking details in multiple countries, enabling clients to pay them as though they were domestic contractors.

Managing International Cash Flow More Efficiently

Remote workers are also beginning to use multi-currency accounts as operational business tools rather than simple payment wallets. A freelance videographer may receive payments in EUR, pay editing contractors in PHP (Philippine Peso), and subscribe to software billed in USD. Without a multi-currency system, each transaction creates another conversion layer and additional fees. Centralizing these flows inside one platform reduces “conversion chaining,” where money is repeatedly exchanged across currencies before final use.

There is also a growing distinction between traditional bank-based multi-currency accounts and fintech platforms. Traditional banks generally offer stronger regulatory protections and integrated banking services, but fintech providers tend to outperform them in transparency and exchange-rate efficiency. Recent industry comparisons show that platforms such as Wise and Revolut emphasize mid-market exchange rates, while many conventional banks still apply opaque spreads that users only notice after comparing final payouts.

A practical issue rarely discussed is “conversion fatigue.” Remote workers handling several currencies often experience budgeting confusion because income, taxes, and expenses are all denominated differently. Reddit discussions among digital nomads frequently highlight the administrative burden of manually tracking multiple exchange rates across months. One emerging solution is maintaining a “base currency” for accounting purposes while preserving balances in original currencies until needed. This simplifies tax reporting and provides clearer financial visibility.

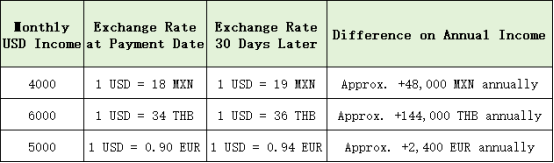

Here is an example of how exchange timing alone can influence annual income:

For many remote workers, the biggest savings no longer come solely from reducing transfer fees. They come from strategic timing, currency diversification, and separating earning currencies from spending currencies. That mindset transforms multi-currency banking from a convenience feature into a financial optimization strategy.

Practical Tips for Remote Workers

First, identify your core currencies. Receiving frequent payments in USD, EUR, and GBP? Choose an account that supports all three and offers minimal conversion fees. Next, monitor exchange rates. Many multi-currency accounts allow automated notifications or “rate alerts,” so you can convert funds when rates are favorable.

Another tip is to consolidate payments. Instead of multiple small transfers, waiting for a larger lump sum can reduce per-transaction fees. Additionally, link your multi-currency account with payment platforms and local bank accounts to simplify transfers and reduce the need for physical withdrawals abroad.

Finally, document your transactions. For tax purposes, holding multiple currencies can complicate reporting, but most multi-currency accounts provide detailed statements, making it easier to track gains and losses and comply with local regulations.

(This article is for informational purposes only and does not constitute financial advice. Readers should consult a professional financial advisor regarding their specific circumstances.)

FAQs

Q1: Can multi-currency accounts handle cryptocurrency?

Most traditional multi-currency accounts do not support cryptocurrencies. Specialized crypto wallets are required for that purpose.

Q2: Are multi-currency accounts safe for large balances?

Yes, as long as you use regulated banks or financial platforms insured under local banking laws. Always verify the platform’s regulatory status.

Q3: Do multi-currency accounts affect taxes?

They may. Holding multiple currencies can complicate reporting, but detailed transaction records provided by the account can help streamline reporting.

About Author

Alex Mercer is a financial strategist specializing in digital nomad and freelance economies. With over a decade of experience advising remote workers on banking solutions, currency management, and cross-border financial planning, Alex combines practical insights with real-world examples to help readers maximize income and minimize hidden fees.

References

[1] Wise. (2023). Currency conversion fees explained.

[2] TransferWise. (2023). How to save on currency exchange for freelancers.

Maximize your earnings and reduce hidden costs by exploring more practical finance strategies on this blog—you never know what savings you’re missing!

Recommend:

How Student Loan Forgiveness Can Become a Down Payment for Real Estate Investing

The Self-Employed Guide to Safe, Smart Retirement Contributions

Snowball vs Avalanche Method: Which Debt Repayment Strategy Works Best for You?

Funding Your Child’s College with Tax-Free Income: A Practical Guide to Short-Term Municipal Bonds