May 5, 2026

Key Highlights:

● BNPL apps can accumulate high-interest debt quickly, creating a financial trap.

● Low-interest personal loans offer a way to consolidate multiple BNPL debts into one manageable payment.

● Consolidating debt with a personal loan can help protect your credit score if done carefully.

● Planning repayment schedules and understanding loan terms are crucial to avoid further debt.

● This approach provides a realistic path to regain control over finances without drastic lifestyle changes.

Estimated Reading Time: 9 minutes┃Post by: Jordan Hayes

Buy Now, Pay Later (BNPL) services have grown exponentially, offering convenience and instant gratification. Platforms like Klarna, Afterpay, and Affirm allow consumers to split purchases into smaller installments, often interest-free if paid on time. However, real-life scenarios reveal a common problem: multiple small debts can quickly add up. For example, consider a consumer who makes six BNPL purchases in one month, each costing $200, with a late fee of $10 per missed payment. Missing even a single payment across multiple accounts can lead to $60 in fees, while interest can accrue on longer delays, pushing the total owed beyond the original $1,200.

This small-debt accumulation is not always visible in monthly budgets, and the fragmented nature of BNPL payments can cause missed deadlines, stress, and, in some cases, a drop in credit score if the provider reports late payments to credit bureaus. Many consumers are caught unaware, assuming that small, installment-based debt is harmless.

Using Low-Interest Personal Loans to Consolidate BNPL Debt

A strategic solution is using a low-interest personal loan to consolidate multiple BNPL balances into a single payment. The goal is simple: replace higher-cost, fragmented debt with one manageable, predictable payment while minimizing potential damage to your credit score.

Imagine a consumer with $1,500 spread across five BNPL platforms, each charging $15–$20 in late fees monthly. If they obtain a personal loan for $1,500 at a 9% annual interest rate over 12 months, the monthly payment becomes approximately $132. In contrast, BNPL late fees alone could escalate to $75–$100 monthly if multiple payments are missed.

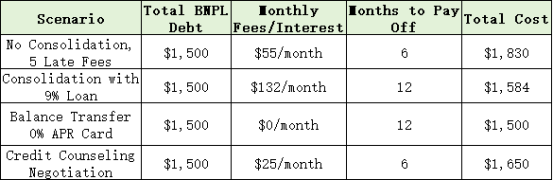

Real-Life Scenario Table

By consolidating into a $1,500 personal loan at 9% interest, the total repayment over 12 months would be $1,584, saving $91 while creating a structured, predictable repayment schedule.

Protecting Your Credit Score While Consolidating

The key to using a personal loan effectively is to handle the transition responsibly. Opening a new loan generates a hard inquiry, which may cause a minor temporary dip in your credit score. However, consolidating debt can improve your credit utilization ratio by reducing outstanding revolving debts. Timely repayment of the personal loan, unlike the fragmented BNPL payments, helps build a positive repayment history.

Consider a practical timeline:

● Month 1: Obtain the loan, pay off all BNPL balances. Credit score may dip by 2–5 points due to the inquiry.

● Months 2–12: Make on-time monthly payments on the personal loan. The improved credit utilization ratio may gradually increase the score by 5–10 points over the year.

Maintaining open communication with lenders is crucial. Some BNPL providers offer temporary hardship programs. Combining those options with a personal loan strategy ensures both financial flexibility and credit protection.

Behavioral Traps Behind BNPL Usage

Many consumers underestimate the cumulative impact of BNPL purchases due to psychological discounting. Splitting payments into small installments can create the illusion that the debt is smaller than it really is. Research shows that people tend to focus on the immediate affordability of $50/month rather than the aggregate $600 owed.

Consider a real-world scenario: Emma uses BNPL for five clothing purchases totaling $800 over two months. Even though each installment is $80, she perceives the expense as minor. However, once unexpected bills arrive—car repairs or medical expenses—she may miss payments on one or more BNPL platforms, triggering fees and interest.

Addressing this behavioral trap requires visibility and budgeting discipline. A simple method is to create a debt dashboard that lists all BNPL balances, due dates, fees, and interest rates. Visualizing the cumulative debt often motivates faster repayment or consolidation.

Illustrative Data Table: Cost Comparison of BNPL vs. Consolidation

This table illustrates that while personal loans are effective, alternatives may provide slightly better or worse outcomes depending on timing, fees, and credit access.

Mitigating Long-Term Risk

Consolidation solves immediate payment issues, but preventing future BNPL debt accumulation is equally critical. Some practical tips:

Freeze BNPL accounts temporarily: Many apps allow account suspension or temporarily disabling payment options.

Budget for ‘deferred spending’: Before using BNPL, allocate funds in your monthly budget for repayment.

Use BNPL strategically: Only for planned, essential purchases where installment payments are manageable without affecting other obligations.

Emergency Fund Cushion: Maintaining even a small emergency fund (e.g., $500–$1,000) reduces the likelihood of missed BNPL payments during unexpected expenses.

Practical Tips for Implementation

Review all BNPL balances, including upcoming payments and late fees.

Compare personal loan offers, focusing on interest rates, fees, and repayment flexibility.

Avoid taking on additional BNPL purchases during consolidation.

Automate loan payments to avoid missing a due date.

Track progress monthly to adjust your budget and stay ahead of repayments.

This approach requires discipline, but it creates a realistic path to eliminating high-interest BNPL debt without triggering significant credit damage.

(This article is for informational purposes only and does not constitute financial advice. Readers should consult with a qualified financial advisor before making any financial decisions.)

FQAs

Q1: Will consolidating BNPL debt with a personal loan always improve my credit score?

Not necessarily. While consolidation can help reduce credit utilization and create predictable payments, opening a new loan may temporarily lower your score. Long-term improvement depends on consistent, on-time repayments.

Q2: Can I consolidate BNPL debts if one of my accounts is already late?

Yes, but it’s important to address late fees immediately and communicate with the BNPL provider. A personal loan can help pay off past-due balances, preventing further credit reporting damage.

Q3: What if I can’t qualify for a low-interest personal loan?

Alternatives include negotiating payment plans with BNPL providers, using balance transfer credit cards with introductory 0% APR offers, or seeking credit counseling services.

About Author

Jordan Hayes is a personal finance consultant specializing in debt management and credit optimization. With over 10 years of experience guiding consumers through complex financial decisions, Jordan focuses on actionable strategies to regain control over finances and protect credit scores.

References

[1] World Finance. (2023). Why GDP is no longer the most effective measure of economic success.

[2] NerdWallet. (2024). How to consolidate debt with a personal loan.

[3] Experian. (2023). Understanding how BNPL affects your credit score.

Stay on our blog to explore more actionable tips for managing personal finances in a modern, credit-driven world.

Recommend:

The Gig Worker’s Guide to Lowering Estimated Taxes With Investment Losses

How to Improve Your Credit Score?

Why Your Paycheck Disappears Before Rent?

The Self-Employed Guide to Safe, Smart Retirement Contributions