May 6, 2026

Key Takeaways:

● A good credit score is essential for loans, insurance, and financial opportunities.

● Consistent financial habits are more effective than drastic changes.

● Monitoring your credit report helps prevent errors and detect fraud.

● Responsible use of credit cards and loans demonstrates reliability.

● Patience and persistence are key to steadily improving your credit score.

Estimated Reading Time: 15 minutes┃Post by: Jessica L. Carter

Your credit score is a central measure of your financial health. It influences your ability to borrow money, the interest rates you pay, and even some employment opportunities. Many beginners think improving credit requires complex financial strategies, but the reality is that consistent, straightforward actions produce lasting results.

1. Understand Your Credit Report

The first step in improving your credit is understanding your current situation. Obtain your credit reports from Equifax, Experian, and TransUnion. These reports detail your accounts, payment history, outstanding debt, and any public records like liens or bankruptcies.

Key Actions:

● Review all accounts and balances for accuracy.

● Look for errors or outdated information and dispute inaccuracies with the credit bureau.

● Note trends in your payment behavior and account utilization.

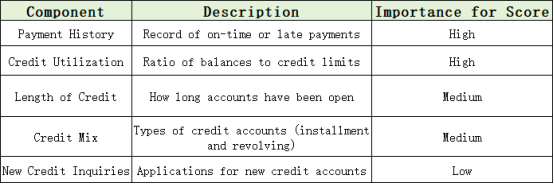

Table: Key Components of a Credit Report

Understanding these components helps you identify which areas require attention.

2. Make Timely Payments

Payment history is the single most important factor in your credit score. Late or missed payments can have a lasting negative impact.

Best Practices:

● Always pay at least the minimum on time.

● Set up automatic payments or calendar reminders to prevent missed deadlines.

● If payments are occasionally missed, bring accounts current as soon as possible.

Consistency in timely payments signals reliability to lenders and has a compounding positive effect on your score over time.

3. Manage Credit Utilization

Credit utilization—the percentage of available credit you are using—affects roughly 30% of your credit score. Lower utilization ratios indicate responsible borrowing behavior.

Best Practices:

● Aim to keep your utilization below 30% across all revolving accounts.

● Prioritize paying down high-balance accounts to reduce utilization.

● Avoid closing accounts solely to manage debt, as this can increase your utilization ratio.

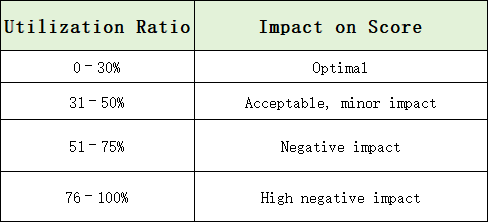

Table: Credit Utilization Guidelines

Maintaining low utilization consistently over months improves your credit profile gradually.

4. Limit New Credit Applications

Hard inquiries from new credit applications can temporarily lower your score. Each inquiry signals potential financial risk to lenders.

Best Practices:

● Apply for new credit only when necessary.

● Space out applications over several months to minimize impact.

● Consider prequalification tools that perform soft inquiries, which do not affect your score.

Monitoring the frequency of applications protects your score while ensuring access to credit when needed.

5. Diversify Your Credit Mix

Credit scoring models favor borrowers who manage multiple types of credit, such as revolving accounts (credit cards) and installment loans (student loans, auto loans, personal loans).

Best Practices:

● Maintain a healthy mix of credit types without overextending yourself.

● Avoid taking new loans purely to diversify; the goal is responsible, manageable credit.

● Monitor how different account types affect your overall score.

A diversified credit profile demonstrates to lenders that you can handle various financial obligations responsibly.

6. Monitor Credit Reports and Scores Regularly

Regular monitoring helps detect errors, fraudulent activity, and trends in your credit score.

Best Practices:

● Check your credit reports at least once a year from all three major bureaus.

● Use free monthly credit monitoring services to track changes over time.

● Immediately dispute unauthorized activity or discrepancies to prevent long-term damage.

Maintaining awareness of your credit activity allows proactive adjustments to your financial habits.

7. Be Patient and Consistent

Credit improvement is a gradual process. Scores do not increase overnight, but steady, responsible behavior compounds into significant gains over time.

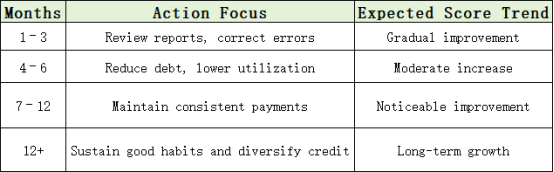

Recommended Timeline for Improvement:

Consistency in financial behavior is more effective than temporary, large-scale interventions.

8. Practical Implications: How Credit Affects Costs

A higher credit score can reduce interest rates on loans, saving significant money over time. Even modest improvements can have tangible financial benefits.

Table: Loan Rates by Credit Score

Maintaining a strong credit profile directly reduces borrowing costs, making credit improvement a financially strategic goal.

Improving your credit score is a combination of understanding your financial profile, maintaining responsible habits, and making informed decisions over time. By reviewing your reports, making timely payments, managing debt, limiting new credit, diversifying your accounts, and monitoring activity, you build a credit history that reflects reliability and financial health. The process requires patience, but the benefits—lower interest rates, better loan approvals, and financial security—are substantial.

(This article is for educational purposes only and does not constitute personalized financial, legal, or investment advice. While the strategies presented are based on widely accepted financial principles, individual circumstances vary, and readers should consult licensed financial advisors or credit professionals before making decisions affecting their credit, debt, or finances. The author and blog are not liable for any actions taken based on this content, and no specific product, service, or company mentioned is endorsed.)

FAQs

Q1: How long does it take to improve a credit score?

Minor improvements can occur in 1–3 months, while significant changes may take 6–12 months of consistent behavior.

Q2: Will closing old accounts help my score?

Generally no; closing accounts can reduce available credit and increase utilization, potentially lowering your score.

Q3: Does checking my own credit hurt my score?

No. Personal checks are soft inquiries and do not impact your credit score.

About the Author

Jessica L. Carter is a certified financial coach with over a decade of experience helping individuals improve credit, manage debt, and build financial security. She specializes in translating complex financial concepts into practical, actionable steps for beginners and contributes to financial literacy blogs, workshops, and educational resources aimed at empowering readers to take control of their finances.

References

[1] Experian. (2023). How to improve your credit score.

[2] FICO. (2023). What’s in my credit score?

[3] Consumer Financial Protection Bureau. (2023). Credit reports and scores.

Stay on this blog for more beginner-friendly personal finance strategies to take control of your money and secure a better financial future.

Recommend:

Funding Your Child’s College with Tax-Free Income: A Practical Guide to Short-Term Municipal Bonds

Budget vs Expense Tracking: Understanding the Difference and Why You Need Both

Common Budgeting Mistakes and How to Avoid Them

Budgeting for College Students: How to Stretch Every Dollar